Ultimate Beginner’s Guide to Investing: Steps to Achieve Financial Freedom

Introduction: Your Financial Freedom Story Starts NOW

Let’s be real for a second. Does the thought of investing make your palms a little sweaty? Do you see terms like ETFs and compound interest and just… scroll faster? You’re not alone. I’ve been there, staring at a screen full of stock charts that looked like a secret code I was never meant to crack.

But what if I told you that cracking that code is the single most powerful thing you can do to build the life you want? That’s right—we’re talking about financial freedom. Not just having “enough,” but having the power to make choices based on your dreams, and not your bank account balance.

This Ultimate Beginner’s Guide to Investing is your personal GPS on that journey. We’re going to cut through the noise, ditch the intimidating jargon, and break down the steps to achieve financial freedom into a simple, actionable plan. Forget what you’ve heard about needing thousands to start or being a Wall Street wizard. My goal is to show you exactly how to start investing, even with just a few dollars, and build a future that excites you.

So, follow me. Your journey to becoming an investor starts here. Let’s turn your financial stress into financial success. SERIOUSLY!

1. Understanding Investing and Financial Freedom

Let me paint you a picture: financial freedom isn’t about being filthy rich or buying yachts (though hey, if that’s your thing, go for it). It’s about waking up one day and realizing you don’t HAVE to work for money anymore. Your money works for you instead.

What “Financial Freedom” Really Means

Financial freedom means your investments generate enough passive income to cover your living expenses. Simple as that. You’re not chained to a 9-to-5 job you hate. You can travel for three months if you want. You can start that passion project without worrying about the paycheck.

I like to think of it as buying back your time. When I started my investing journey, my goal wasn’t to become a millionaire—it was to have OPTIONS. And guess what? That’s way more achievable than you think.

Here’s what financial freedom looks like in real numbers:

| Your Monthly Expenses | Investment Income Needed | Approximate Portfolio Size (4% rule) |

| $2,000 | $2,000/month | $600,000 |

| $3,500 | $3,500/month | $1,050,000 |

| $5,000 | $5,000/month | $1,500,000 |

Don’t freak out at those numbers. We’re building toward this, not winning the lottery tomorrow.

Why Investing is Essential for Achieving Financial Independence

Here’s the brutal truth: you cannot save your way to financial freedom. I’ll say it louder for the people in the back—SAVING ALONE WON’T GET YOU THERE.

Why? Inflation. That sneaky wealth killer sitting at around 3% annually. Your savings account earning 0.5%? You’re actually LOSING 2.5% of your purchasing power every year. It’s like running on a treadmill while someone slowly turns up the speed.

Investing changes the game completely. The stock market has averaged about 10% annual returns over the past century. Let me show you what this means:

The Power of Investing vs. Saving:

- Save $500/month at 0.5% interest for 30 years = $185,000

- Invest $500/month at 8% average return for 30 years = $745,000

That’s a difference of $560,000! Same money, wildly different outcomes.

I invested $3,000 in an S&P 500 index fund back in 2015. I didn’t touch it, didn’t panic during market dips, just let it ride. Today? It’s worth over $8,500. My savings account during the same period? It grew by maybe $200. The math doesn’t lie.

Common Myths About Investing That Hold Beginners Back

Alright, let’s bust some myths that are keeping you broke:

Myth #1: “You need a lot of money to start investing”

WRONG. You can literally start with $5 using apps like Acorns. I know people who began with spare change from rounding up purchases. Stop waiting for the “perfect amount”—that day never comes.

Myth #2: “Investing is the same as gambling”

Nope. Gambling is random chance. Investing is buying ownership in actual companies that produce real products and generate real profits. When you invest in Apple, you own a tiny piece of a company worth trillions. That’s not a casino bet.

Myth #3: “You need to be an expert or constantly watch the market”

Total nonsense. Warren Buffett himself recommends most people invest in low-cost index funds and ignore the daily noise. I check my portfolio maybe once a month. You don’t need a finance degree—you need a solid strategy and patience.

Myth #4: “The stock market is too risky for beginners”

Yes, there’s risk. But you know what’s riskier? Staying broke forever. Besides, there are conservative investment options for beginners that balance risk and reward beautifully.

Myth #5: “I’ll start investing when I make more money”

This is the biggest trap. The best time to start was yesterday. The second-best time is TODAY. Time in the market beats timing the market every single time.

Pro Tip: The people who wait for “perfect conditions” are the same ones still waiting 20 years later. Start small, start now, start imperfectly—just START.

2. How to Start Investing (Even with Little Money)

Ready to actually DO this? Good. Because knowing without action is just expensive entertainment. Let’s get your money working for you.

Steps to Take Before Your First Investment

Hold up—before you throw money at the stock market, we need to handle some housekeeping. Trust me on this.

Step 1: Get Your Financial House in Order

Look at your current situation honestly. Do you have high-interest debt? Credit cards charging 20%? Pay those off first. There’s no investment that’ll consistently beat a 20% return, so killing that debt IS your best investment right now.

Step 2: Build a Baby Emergency Fund

Aim for $1,000 to start. This prevents you from selling investments when your car breaks down or your laptop dies. I learned this the hard way when I had to sell stocks at a loss because my emergency fund was… zero.

Step 3: Educate Yourself (But Don’t Overdo It)

Read a few books, watch some YouTube videos, but don’t fall into “analysis paralysis.” You don’t need to understand every financial term—you need to understand the basics and take action.

How to Set Clear Financial Goals

Vague goals create vague results. “I want to be rich” doesn’t cut it. Get SPECIFIC.

Here’s my framework:

Short-term goals (1-3 years):

- Build a $10,000 emergency fund

- Save for a down payment on a car

- Fund a vacation without debt

Medium-term goals (3-10 years):

- Save $50,000 for a house down payment

- Build a portfolio worth $100,000

- Generate $500/month in passive income

Long-term goals (10+ years):

- Achieve financial independence

- Build a $1 million portfolio

- Retire early or work because you WANT to

Write these down. Put them where you’ll see them daily. Your goals should excite you AND scare you a little.

How Much Money Do You Really Need to Start?

The honest answer? As little as $1. Seriously.

Here’s the breakdown:

| Platform | Minimum Investment | Best For |

| Acorns | $5 | Absolute beginners, micro-investing |

| Robinhood | $1 | Fractional shares, individual stocks |

| M1 Finance | $100 | Automated portfolios, long-term |

| Fidelity | $0 | Index funds, comprehensive tools |

| Vanguard | $1,000 (some funds) | Serious long-term investors |

I started with $50 in Robinhood. Bought a fractional share of Amazon. Watched it grow. Added more when I could. No shame in starting small—the shame is in never starting.

Best Beginner-Friendly Investment Platforms

Let me break down the platforms I actually recommend:

Robinhood – Perfect if you want simplicity. Commission-free trades, clean interface, great for learning. Just don’t get sucked into day trading.

Acorns – This app rounds up your purchases and invests the spare change. Bought coffee for $3.50? It rounds to $4 and invests $0.50. Genius for beginners who “can’t afford” to invest.

M1 Finance – My personal favorite for automation. You build a “pie” of investments, and it automatically rebalances. Set it and forget it.

Fidelity – Offers amazing research tools and zero expense ratio index funds (FZROX). Great for serious beginners ready to go deep.

Pro Tip: Don’t open accounts on five different platforms. Pick ONE, master it, then expand if needed.

3. Building a Strong Financial Foundation

You can’t build wealth on a shaky foundation. I’ve seen people invest aggressively while drowning in debt and wonder why they’re not getting ahead. Let’s fix that.

The Link Between Budgeting, Saving, and Investing

These three work together like a well-oiled machine. You can’t skip steps.

Budgeting tells your money where to go instead of wondering where it went. I use the 50/30/20 rule:

- 50% for needs (rent, food, utilities)

- 30% for wants (fun stuff, entertainment)

- 20% for savings and investments

When I first budgeted properly, I found $400 a month I didn’t know I had. That went straight into investments.

Saving builds your safety net and investment capital. But remember—savings are for SHORT-term goals and emergencies. Everything else? Invest it.

Investing multiplies your saved money through compound growth. It’s the ENGINE that drives wealth building.

Setting Up an Emergency Fund Before Investing

Real talk: do NOT invest your emergency fund. I don’t care how good that stock tip sounds.

Your emergency fund needs to be:

- Liquid (accessible within 24 hours)

- Safe (no market risk)

- Boring (high-yield savings account, that’s it)

How much you need:

- Minimum: 3 months of expenses

- Ideal: 6 months of expenses

- Freelancers/self-employed: 12 months of expenses

I keep mine in a Marcus by Goldman Sachs high-yield savings account. It earns around 4% right now—(Although can fluctuate) way better than traditional banks—but it’s still SAFE.

Managing Debt While Building Wealth

Can you invest while paying off debt? Sometimes yes, sometimes no.

High-interest debt (>7% interest): Pay this off FIRST. Credit cards, personal loans, payday loans—crush these before investing. They’re wealth destroyers.

Low-interest debt (<4% interest): You can invest while paying this off. Mortgages, student loans, car payments at low rates—pay the minimums and invest the rest.

Medium-interest debt (4-7%): This is the gray area. My approach? Split it. Put 60% toward debt, 40% toward investing. You’re making progress on both fronts.

Pro Tip: Automate everything. Set up automatic payments for debt and automatic transfers to investment accounts. Remove the decision-making—just let it happen.

The goal is to stop the financial bleeding (high-interest debt) so your investments can flourish.

Next, we’ll dive into the fun part: the actual investment strategies and options you can choose from to make your money grow!

4. Choosing the Right Investment Strategy

Here’s where most beginners get overwhelmed and quit. They think they need some complex strategy that requires a finance PhD. Spoiler alert: you don’t. You need a strategy that matches YOUR goals and YOUR lifestyle.

Long-term vs Short-term Investing Explained

Let me be blunt: short-term investing is for experienced traders, not beginners trying to build wealth. I’ve watched too many friends lose money trying to “flip” stocks quickly.

Short-term investing (days to months):

- Requires constant monitoring

- Higher stress, higher fees

- Timing the market (which even pros fail at)

- Tax implications eat your profits

- Honestly? It’s exhausting

Long-term investing (5+ years):

- Set it and forget it approach

- Lower stress, lower fees

- Time IN the market wins

- Better tax treatment

- Actually lets you sleep at night

I tried day trading once. Made $200, felt like a genius. Lost $800 the next week, felt like an idiot. Learned my lesson and switched to long-term investing. Best decision ever.

The numbers don’t lie:

| Strategy | Average Annual Return | Time Commitment | Beginner Success Rate |

| Short-term trading | Variable (-20% to +50%) | 10-40 hours/week | 10-20% |

| Long-term investing | 8-10% historically | 1 hour/month | 70-80% |

For beginners, long-term investing wins every single time. We’re building wealth, not gambling.

Active vs Passive Investing: Which is Better for Beginners?

This debate is like asking whether you should cook gourmet meals or use a slow cooker. Both work, but one requires way more effort.

Active investing means:

- Picking individual stocks

- Trying to beat the market

- Researching companies constantly

- Higher fees (if using fund managers)

- Requires significant time and knowledge

Passive investing means:

- Buying index funds or ETFs

- Matching market returns (not beating them)

- Minimal research needed

- Lower fees

- Set it and literally forget it

Here’s the kicker: Studies show that 90% of active fund managers fail to beat the market over 15 years. Even the “experts” can’t consistently win. So why would you try?

I invest 95% of my portfolio passively through index funds. The other 5%? That’s my “fun money” for individual stocks I believe in. This balance keeps me engaged without risking my financial future.

Pro Tip: Start 100% passive. Once you have $10,000+ invested and understand the market better, THEN consider allocating 5-10% to active picks if you want.

How to Create an Investment Plan That Fits Your Goals

Time to get tactical. Here’s my framework for building YOUR personalized investment plan:

Step 1: Define Your Timeline

- Retiring in 30 years? Aggressive growth stocks

- Buying a house in 5 years? Balanced mix with some bonds

- Need money in 2 years? Don’t invest it—save it

Step 2: Assess Your Risk Tolerance

Ask yourself: “If my portfolio dropped 30% tomorrow, would I panic sell or buy more?”

If you’d panic—you need a conservative portfolio. If you’d buy more—you can handle aggressive growth.

Step 3: Choose Your Asset Allocation

Here’s my recommended split by age:

| Age Range | Stocks | Bonds | Strategy |

| 20-30 | 90% | 10% | Maximum growth |

| 31-40 | 80% | 20% | Aggressive growth |

| 41-50 | 70% | 30% | Moderate growth |

| 51-60 | 60% | 40% | Conservative growth |

| 61+ | 50% | 50% | Capital preservation |

Step 4: Automate Everything

Set up automatic monthly investments. Same day, same amount, every month. Remove emotions from the equation.

My investment plan is simple:

- $500/month to Vanguard Total Stock Market Index

- $200/month to international index fund

- $100/month to bond fund

- Rebalance once per year

That’s it. No complexity, no stress, just consistent wealth building.

5. Exploring the Best Investment Options for Beginners

Now we’re getting to the good stuff. Let’s talk about WHERE to actually put your money. These are the vehicles that’ll carry you to financial freedom.

5.1 Stocks and ETFs

What Are Stocks?

When you buy a stock, you’re buying a tiny piece of a company. You become a part-owner. If the company grows and profits, your share value increases. If it tanks, so does your investment.

Think of it like this: You buy one share of Microsoft at $400. Microsoft releases an amazing new product, demand explodes, stock price hits $500. You just made $100 (minus taxes). Simple.

But here’s the catch—individual stocks are risky. One bad quarterly report and your stock can drop 20% overnight. That’s why beginners shouldn’t go all-in on individual stocks.

What Are ETFs and Why Beginners Should Consider Them

ETFs (Exchange-Traded Funds) are like buying a basket of stocks in one purchase. Instead of putting all your money on one company, you spread it across hundreds.

Why ETFs are PERFECT for beginners:

- Instant diversification (one purchase = hundreds of companies)

- Low fees (often under 0.1% annually)

- Trade like stocks (buy/sell anytime)

- Professionally managed

- Lower risk than individual stocks

I love ETFs because they remove the stress of picking winners. You’re basically betting on the entire economy growing—which it has for over a century.

Example: Vanguard Total Stock Market ETF (VTI)

VTI is my go-to recommendation for beginners. Here’s why:

- Holds over 3,500 U.S. stocks

- Expense ratio: 0.03% (basically free)

- Covers entire U.S. market

- Historical returns: ~10% annually

- One purchase = complete diversification

I’ve held VTI since 2016. Through market crashes, pandemics, and chaos—it’s consistently grown. It’s boring, reliable, and exactly what beginners need.

5.2 Mutual Funds and Index Funds

Difference Between Mutual Funds and Index Funds

These terms confuse everyone, so let me clarify:

Mutual Funds:

- Actively managed by professionals

- Try to beat the market

- Higher fees (1-2% annually)

- Minimum investments often $1,000-$3,000

Index Funds:

- Track a specific market index (like S&P 500)

- Passively managed

- Ultra-low fees (0.03-0.2%)

- Better long-term performance

Both are mutual funds technically, but index funds follow a specific strategy of matching—not beating—the market.

The data is clear: Index funds outperform 90% of actively managed mutual funds over time. Lower fees + market returns = more money for you.

Best Low-Cost Funds for Beginners

Here are my top picks:

FZROX (Fidelity ZERO Total Market Index):

- Expense ratio: 0.00% (literally zero fees)

- Tracks entire U.S. market

- Minimum investment: $0

- It’s basically free money management

FXAIX (Fidelity 500 Index Fund):

- Expense ratio: 0.015%

- Tracks S&P 500

- Proven long-term performance

- Warren Buffett’s recommendation

Pro Tip: These low fees matter MORE than you think. A 1% fee vs. 0.1% fee over 30 years can cost you hundreds of thousands of dollars.

5.3 Bonds and Real Estate

Bonds for Stability and Passive Income

Bonds are the “boring but reliable” cousin of stocks. You’re essentially lending money to companies or governments, and they pay you interest.

Why bonds matter:

- Provide stability when stocks crash

- Generate predictable income

- Lower risk (especially government bonds)

- Balance your portfolio

I keep 20% of my portfolio in bonds. They won’t make me rich, but they help me sleep well during market volatility.

Best bond options for beginners:

- AGG (iShares Core U.S. Aggregate Bond ETF)

- BND (Vanguard Total Bond Market ETF)

- U.S. Treasury bonds (safest option)

Real Estate Investing Basics

Real estate builds wealth, but buying rental properties requires huge capital. Enter REITs (Real Estate Investment Trusts).

REITs let you invest in real estate with as little as $10. You get:

- Exposure to commercial properties

- Regular dividend payments

- Diversification beyond stocks

- No property management headaches

VNQ (Vanguard Real Estate ETF) is my pick. It holds hundreds of REITs, pays consistent dividends, and requires zero landlord duties.

5.4 Alternative and Emerging Investments

Cryptocurrency Basics for Beginners

Crypto is the wild west. High potential, high risk, high volatility. I’m not anti-crypto, but I’m realistic about it.

My honest take:

- Invest only 5% max of your portfolio

- Stick to Bitcoin and Ethereum (ignore random coins)

- Expect extreme volatility

- Never invest money you can’t afford to lose

I’ve made money on crypto. I’ve also watched it drop 60% in weeks. It’s NOT for the faint-hearted or your retirement fund.

ESG Investing: What It Means and How to Get Started

ESG (Environmental, Social, Governance) investing lets you make money while supporting companies that align with your values.

ESG funds focus on:

- Environmental sustainability

- Social responsibility

- Ethical governance

Popular options include VFTAX (Vanguard FTSE Social Index Fund) and ESGU (iShares ESG Aware MSCI USA ETF).

I allocate 10% to ESG because I want my money supporting companies building a better future.

6. The Power of Compound Interest

This is where the magic happens. Einstein allegedly called compound interest the “eighth wonder of the world.” He wasn’t exaggerating.

How Compounding Grows Your Wealth Faster

Compound interest means you earn returns on your returns. Your money makes money, then THAT money makes money. It’s a snowball effect that gets exponentially powerful over time.

Here’s the simple formula: You invest money → It grows → The growth gets reinvested → It grows MORE → Repeat forever.

The longer you invest, the more dramatic compounding becomes. It starts slow, then suddenly explodes.

Simple Illustration of Compounding Returns Over Time

Let me show you real numbers that’ll blow your mind:

Scenario: Investing $500/month at 8% annual return

| Years | Total Invested | Portfolio Value | Growth from Compounding |

| 5 | $30,000 | $36,738 | $6,738 |

| 10 | $60,000 | $91,473 | $31,473 |

| 20 | $120,000 | $294,510 | $174,510 |

| 30 | $180,000 | $745,179 | $565,179 |

| 40 | $240,000 | $1,745,503 | $1,505,503 |

See what happened? In the first 10 years, you made $31K from compounding. In years 30-40, you made over $1 MILLION from compounding. Same monthly investment, wildly different results because of TIME.

This is why starting early is EVERYTHING. A 25-year-old investing $300/month will have more at 65 than a 35-year-old investing $600/month. Time beats money every time.

Pro Tip: Never withdraw your investment gains. Let them compound. That’s where real wealth comes from—not your contributions, but the exponential growth of reinvested returns.

The takeaway is simple: Start NOW. Time is your most powerful asset. Every year you wait is a year of compounded growth you can never get back. This is the ultimate wealth-building tip.

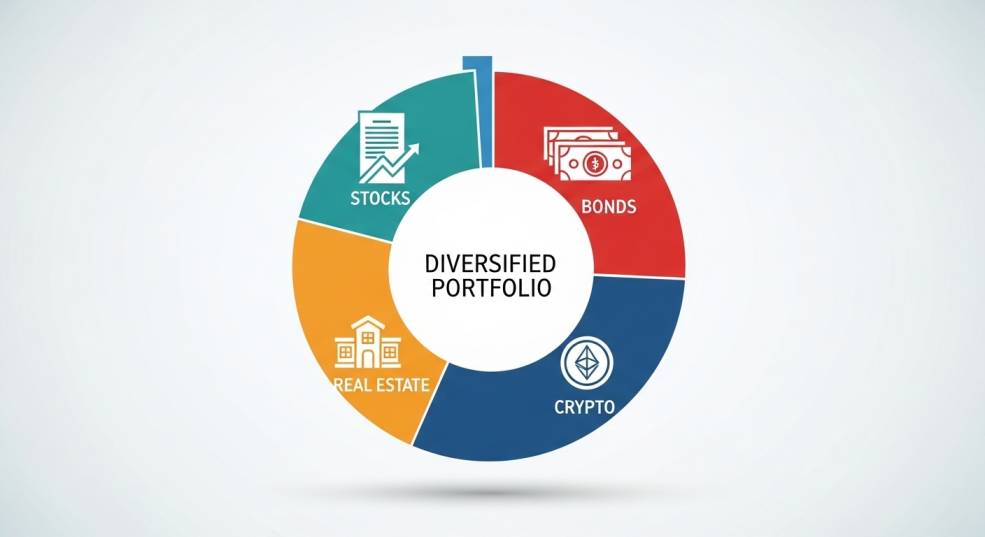

7. Diversifying Your Portfolio

You’ve heard the saying “Don’t put all your eggs in one basket,” right? Well, in investing, that basket could fall off a cliff and take your entire financial future with it. Let’s make sure that doesn’t happen.

Why Diversification Matters

Diversification is your financial safety net. It’s the difference between a bad year and financial catastrophe.

Here’s the brutal reality: Even the best companies can fail. Remember Blockbuster? Kodak? They were giants until they weren’t. If you’d put everything into those stocks, you’d be broke today.

When I diversify, I’m spreading risk across:

- Different companies

- Different industries

- Different countries

- Different asset types

If tech stocks crash but healthcare thrives, my portfolio stays balanced. If U.S. markets struggle but international markets boom, I’m still winning. That’s the power of diversification.

Real-world proof:

During the 2020 pandemic crash, my diversified portfolio dropped 25%. My friend who only owned airline and hotel stocks? Down 70%. Same market, wildly different outcomes.

How to Balance Risk Across Different Investment Types

Balancing risk isn’t about eliminating it—it’s about MANAGING it smartly. Think of your portfolio like a recipe. Too much of one ingredient ruins the whole dish.

The Core Asset Classes:

Stocks (High Risk, High Reward):

- Growth potential: 8-12% annually

- Volatility: Can swing 20-40% yearly

- Best for: Long-term growth

Bonds (Low Risk, Lower Reward):

- Growth potential: 2-5% annually

- Volatility: Minimal

- Best for: Stability and income

Real Estate/REITs (Moderate Risk):

- Growth potential: 6-9% annually

- Volatility: Moderate

- Best for: Diversification and dividends

Cash/Money Market (No Risk, Minimal Reward):

- Growth potential: 0-4% annually

- Volatility: None

- Best for: Emergency funds and short-term goals

My personal allocation framework:

| Risk Tolerance | Stocks | Bonds | Real Estate | Cash |

| Aggressive | 80% | 10% | 10% | 0% |

| Moderate | 60% | 25% | 10% | 5% |

| Conservative | 40% | 40% | 15% | 5% |

I’m currently running a moderate portfolio at 32 years old. As I get older, I’ll shift more toward bonds. But right now? I can handle volatility because time is on my side.

Example of a Well-Diversified Beginner Portfolio

Let me show you EXACTLY what a beginner portfolio should look like. No fluff, just actionable allocation.

The Simple Three-Fund Portfolio (My Favorite for Beginners):

60% – U.S. Total Stock Market (VTI or FZROX)

- Covers entire U.S. economy

- 3,500+ companies

- Your core growth engine

30% – International Stocks (VXUS or FTIHX)

- Non-U.S. companies

- Geographic diversification

- Captures global growth

10% – U.S. Bonds (BND or FXNAX)

- Stability during crashes

- Reduces portfolio volatility

- Peace of mind

Total cost: Under 0.1% in fees annually. That’s basically nothing.

For slightly more advanced beginners, here’s my actual portfolio:

| Investment | Allocation | Purpose |

| VTI (U.S. Stocks) | 50% | Core growth |

| VXUS (International) | 20% | Global exposure |

| VNQ (Real Estate) | 15% | Diversification + dividends |

| BND (Bonds) | 10% | Stability |

| Individual stocks | 5% | Fun/learning |

This portfolio has carried me through market crashes, recessions, and chaos. It works because it’s diversified, low-cost, and doesn’t require constant monitoring.

Pro Tip: Start with the simple three-fund portfolio. Master it for a year. THEN add complexity if you want. Simplicity beats complexity for beginners every single time.

8. Managing Risk and Avoiding Common Mistakes

Let’s talk about the mistakes that’ll cost you thousands—or even tens of thousands—if you’re not careful. I’ve made some of these. Learn from my expensive lessons.

Understanding Investment Risk vs Reward

Every investment has risk. EVERY. SINGLE. ONE. Anyone telling you otherwise is lying or selling something.

The key is understanding the risk-reward tradeoff:

Higher potential returns = Higher risk Lower potential returns = Lower risk

There’s no magic investment giving you 50% returns with zero risk. If someone promises that, RUN.

Risk tolerance check:

Answer honestly:

- Can you watch your portfolio drop 30% without panicking?

- Do you have 10+ years before needing this money?

- Can you sleep at night during market volatility?

If you answered “no” to any of these, you need a more conservative portfolio. There’s zero shame in that. Losing sleep over investments is NOT worth it.

The risk pyramid:

| Risk Level | Investment Type | Potential Return |

| Highest | Individual stocks, crypto | -50% to +100%+ |

| High | Growth stock funds | 8-15% |

| Moderate | Balanced funds, REITs | 6-10% |

| Low | Bond funds | 2-5% |

| Lowest | Savings accounts, CDs | 0-4% |

I keep 90% of my portfolio in moderate-to-high risk investments because I’m young and can recover from losses. My dad keeps 70% in low-to-moderate risk because he’s retiring soon. Different situations, different strategies.

Typical Beginner Mistakes in Stock Investment and How to Avoid Them

Let me save you from the painful lessons I learned the hard way:

Mistake #1: Trying to Time the Market

I tried this. Lost money. The market hit a peak, I thought “It’s gonna crash!” Sold everything. Market went up another 30%. Oops.

Fix: Time IN the market beats TIMING the market. Stay invested, ignore the noise.

Mistake #2: Panic Selling During Crashes

March 2020, markets crashed 35%. My friend sold everything, “locking in” his losses. By December, the market fully recovered. He missed a 70% rebound.

Fix: Crashes are BUYING opportunities, not selling opportunities. If you can’t handle volatility, you’re too aggressive.

Mistake #3: Chasing Hot Stocks

Everyone’s talking about some stock that tripled. You buy in at the peak. It immediately drops 40%. Been there, done that, lost the T-shirt.

Fix: By the time everyone’s talking about it, you’re too late. Stick to your strategy.

Mistake #4: Ignoring Fees

A 1% fee doesn’t sound like much, right? Over 30 years, that 1% fee can cost you $200,000+ compared to a 0.1% fee.

Fix: Choose low-cost index funds. Every percentage point in fees is money stolen from your future.

Mistake #5: Not Diversifying

My cousin put $50,000 into one tech stock. Company got hacked, stock dropped 60%, he lost $30,000 overnight.

Fix: Never put more than 5% of your portfolio in any single stock. Ever.

Mistake #6: Checking Your Portfolio Daily

This creates anxiety and triggers emotional decisions. I used to check mine five times daily. Made stupid trades. Lost money.

Fix: Check monthly at most. Set it, forget it, let compound interest work.

Red Flags for Scams and Misleading “Get Rich Quick” Offers

The investment scam industry is HUGE. They prey on beginners who don’t know better. Here’s how to protect yourself:

Red Flag #1: Guaranteed High Returns

“Guaranteed 20% returns!” is a guarantee you’ll lose money. Nothing in investing is guaranteed except that someone promising guarantees is lying.

Red Flag #2: Pressure to Act NOW

“This opportunity disappears tomorrow!” Real investments don’t have countdown timers. Scammers use urgency to bypass your critical thinking.

Red Flag #3: Complex, Confusing Explanations

If you can’t understand how the investment makes money, it’s probably a scam. Bernie Madoff’s Ponzi scheme worked because nobody understood it.

Red Flag #4: Unsolicited Investment Offers

Someone DMs you on Instagram about “financial freedom”? BLOCK THEM. Legitimate investments don’t recruit through social media DMs.

Red Flag #5: Celebrity Endorsements (Especially Crypto)

Just because a celebrity promotes something doesn’t make it legit. Many get paid to promote garbage investments.

Red Flag #6: “Secret” Investment Strategies

“The rich don’t want you to know this!” Actually, the rich DO want you to know: buy index funds and hold forever. That’s the “secret.”

Pro Tip: If an investment opportunity seems too good to be true, it IS too good to be true. Every. Single. Time.

I almost fell for a “high-yield investment program” promising 5% monthly returns. Did the math—that’s 80% annually. Obviously impossible. My greed almost cost me $5,000. Don’t be me.

9. Tracking and Rebalancing Your Investments

You’ve built your portfolio. Awesome. Now you need to maintain it without becoming obsessed. There’s a balance here, and I’ll show you exactly how.

Best Apps for Tracking Your Portfolio

Tracking your investments shouldn’t be complicated or time-consuming. Here are my top picks:

Personal Capital (My #1 Choice):

- Completely FREE

- Tracks all accounts in one dashboard

- Shows asset allocation automatically

- Provides retirement planning tools

- Gives investment fee analysis

I’ve used Personal Capital for five years. It syncs with all my investment accounts, shows my net worth, and helps me see the big picture instantly.

Mint:

- Free budgeting + basic investment tracking

- Good for beginners

- Links to bank and investment accounts

- Better for overall financial health than deep investment analysis

Empower (formerly Personal Capital Pro):

- Professional-grade tools

- Advanced performance tracking

- Fee analyzer shows hidden costs

Your Brokerage App:

- Fidelity, Vanguard, Schwab all have excellent built-in tracking

- If all your investments are in one place, just use their app

- Free and comprehensive

Pro Tip: Don’t use five different apps. Pick ONE and master it. I check Personal Capital once per month, take five minutes to review, then close it. That’s it.

When and How to Rebalance Your Investments for Long-Term Success

Rebalancing sounds fancy, but it’s simple: getting your portfolio back to your target allocation.

Here’s why you need to rebalance:

Let’s say you want 60% stocks, 40% bonds. After a great year, stocks grew and now represent 75% of your portfolio. You’re now RISKIER than intended.

Rebalancing means selling some stocks and buying bonds to get back to 60/40. You’re literally “selling high” and “buying low” automatically.

When to Rebalance:

Option 1: Calendar Rebalancing (My Method)

- Rebalance once per year

- I do mine every January 1st

- Simple, consistent, no overthinking

Option 2: Threshold Rebalancing

- Rebalance when allocations drift 5%+ from target

- More responsive to market changes

- Requires more monitoring

Option 3: Never Rebalancing

- Honestly? This works too for some people

- Lower maintenance

- Lets winners run

For beginners, I recommend annual rebalancing. It’s simple, effective, and keeps you engaged without being obsessive.

How to Rebalance in 4 Easy Steps:

Step 1: Check your current allocation

- Personal Capital shows this automatically

- Or manually calculate: (Investment value ÷ Total portfolio) × 100

Step 2: Compare to your target

- Target: 60% stocks | Current: 70% stocks = 10% overweight

Step 3: Calculate adjustments needed

- If portfolio is $10,000 and stocks are 10% overweight, you need to move $1,000 from stocks to bonds

Step 4: Make the trades

- Sell overweight assets

- Buy underweight assets

- Or direct new contributions to underweight assets (my preferred method)

Rebalancing Example:

| Asset Class | Target | Current Value | Current % | Action Needed |

| U.S. Stocks | 60% | $7,500 | 75% | Sell $1,500 |

| Bonds | 40% | $2,500 | 25% | Buy $1,500 |

| Total | 100% | $10,000 | 100% | Rebalance |

Tax-Smart Rebalancing Tips:

In taxable accounts:

- Use new contributions to rebalance (avoid selling and triggering taxes)

- Only sell if absolutely necessary

- Wait for long-term capital gains rates (held over 1 year)

In retirement accounts (IRA, 401k):

- Rebalance freely—no tax consequences

- Do all your rebalancing here first

I rebalance exclusively in my Roth IRA to avoid taxes. In my taxable account, I just direct new money to whatever’s underweight.

Pro Tip: Most robo-advisors (Betterment, Wealthfront) rebalance automatically for you. If you want truly hands-off investing, use them. They handle everything while you focus on earning more money to invest.

The goal isn’t perfection—it’s staying on track toward financial freedom. Check in periodically, make small adjustments, then get back to living your life. Your portfolio should work FOR you, not consume your every thought.

Next, we’ll talk about putting it all together for the long haul and how to stay motivated on your path to financial freedom!

10. Tax Tips and Retirement Investing

Nobody likes taxes, but ignoring them is like throwing money in the trash. The IRS is going to take their cut—your job is making sure they take the SMALLEST cut possible. Let me show you how.

Basic Tax Implications of Investing

Here’s what nobody tells you when you start investing: Uncle Sam wants a piece of your gains. But the good news? There are legal ways to minimize what you owe.

Capital Gains Taxes (When You Sell for Profit):

Short-term capital gains (held less than 1 year):

- Taxed as ordinary income

- Could be 22-37% depending on your tax bracket

- Basically, the government PUNISHES short-term trading

Long-term capital gains (held over 1 year):

- Taxed at 0%, 15%, or 20% (way better!)

- Rewards patient investors

- This is why I hold everything long-term

Real example from my life:

I bought stock for $1,000, sold it for $2,000 after 8 months. Profit: $1,000. My tax bill? $220 (22% bracket). Ouch.

My friend bought the same stock, held for 13 months, same $1,000 profit. His tax bill? $150 (15% long-term rate). He saved $70 just by waiting five more months.

Dividend Taxes:

- Qualified dividends: 0-20% (if held over 60 days)

- Non-qualified dividends: Taxed as ordinary income

The Tax-Loss Harvesting Trick:

If you have losses, you can use them to offset gains. Sold one stock for a $3,000 gain and another for a $2,000 loss? You only owe taxes on $1,000. I do this every December to reduce my tax bill.

What is a Roth IRA and Why It’s Great for Beginners

The Roth IRA is hands-down the BEST investment account for beginners. I’m not exaggerating. This thing is a wealth-building MACHINE.

Here’s how it works:

You contribute AFTER-TAX money (money you already paid taxes on). It grows tax-free. You withdraw it in retirement COMPLETELY TAX-FREE. Zero taxes on decades of growth. It’s beautiful.

Why Roth IRAs are perfect for beginners:

Tax-free growth forever:

- Contribute $6,000 annually from age 25-65

- At 8% returns, you’d have $1.8 MILLION

- Traditional account taxes on withdrawal? You’d owe $400K+ in taxes

- Roth IRA taxes on withdrawal? $0

Flexibility:

- Withdraw contributions anytime penalty-free (though I don’t recommend it)

- Use $10,000 for first-time home purchase

- No required minimum distributions (RMDs)

Protection from future taxes:

- If tax rates increase (which they probably will), you’re protected

- You’ve already paid taxes at today’s rates

2025 Contribution Limits:

- $7,000 per year if under 50

- $8,000 if 50 or older

Income limits to contribute:

- Single: Under $161,000

- Married: Under $240,000

I maxed out my Roth IRA every single year since I turned 25. It’s now my largest investment account, and I won’t owe a penny in taxes when I retire. Best financial decision I ever made.

How to open a Roth IRA in 15 minutes:

- Go to Fidelity, Vanguard, or Schwab’s website

- Click “Open a Roth IRA”

- Fill out basic info

- Link your bank account

- Transfer money

- Invest in index funds (FZROX, FXAIX, VTI)

- Set up automatic monthly contributions

- Done!

Pro Tip: Open your Roth IRA TODAY. Even if you only put $50 in initially. The account is free, and starting early is EVERYTHING for compound growth.

Using 401(k)s and IRAs to Build Long-Term Wealth

Retirement accounts are your secret weapons. They give you tax advantages that regular investing accounts simply can’t match.

Traditional 401(k):

Your employer-sponsored retirement plan. Money goes in PRE-TAX, reducing your current taxable income.

The magic of employer matching:

If your company matches 50% up to 6% of salary, that’s FREE MONEY. I contribute exactly enough to get the full match—that’s an instant 50% return you can’t get anywhere else.

My 401(k) strategy:

- Contribute enough to get full employer match

- Max out Roth IRA next

- Then increase 401(k) contributions if possible

Traditional IRA vs Roth IRA:

| Feature | Traditional IRA | Roth IRA |

| Contributions | Pre-tax (tax deduction now) | After-tax (no deduction) |

| Growth | Tax-deferred | Tax-free |

| Withdrawals | Taxed as income | Completely tax-free |

| Best for | High earners now | Young people, lower earners |

| RMDs | Yes (required withdrawals at 73) | Never |

I use both. Roth IRA for long-term tax-free growth. Traditional 401(k) for immediate tax deductions and employer match.

2025 Contribution Limits:

- 401(k): $23,000 annually ($30,500 if over 50)

- IRA (Traditional or Roth): $7,000 annually ($8,000 if over 50)

The Millionaire Retirement Formula:

Max out Roth IRA ($7,000) + Get employer 401(k) match ($3,000) = $10,000 invested annually.

At 8% returns over 35 years? That’s $2.2 MILLION in retirement savings.

Pro Tip: Automate everything. Set up automatic payroll deductions for 401(k) and automatic transfers for Roth IRA. You’ll never “feel” the money leaving, and you’ll build massive wealth effortlessly.

11. Passive Income and Financial Independence

This is where investing gets REALLY exciting. Imagine waking up to money hitting your account while you slept. That’s passive income, and it’s the ultimate goal of financial independence.

How Passive Income Supports Financial Freedom

Active income requires your time. You work an hour, you get paid. Stop working, stop getting paid. That’s the trap most people are stuck in.

Passive income breaks that cycle. Your money works while you sleep, vacation, or binge-watch Netflix. It’s the difference between trading time for money and having money work FOR you.

The Financial Independence Number:

Calculate your annual expenses, multiply by 25. That’s your FI number.

- Annual expenses: $40,000

- FI number: $1,000,000 ($40,000 × 25)

Once your investments hit $1 million, you can safely withdraw $40,000 annually (4% rule) without depleting your principal. You’re financially free.

Note: The 4% rule is presented as gospel, but recent research suggests 3-3.5% might be safer.

I’m currently at 30% of my FI number. My passive income covers my rent. Next milestone? Covering all my living expenses. The freedom that brings is INCREDIBLE.

Best Passive Income Ideas for Beginners

Let’s talk about actual, practical ways to generate passive income through investing. No MLM schemes, no “get rich quick” garbage—just real strategies that work.

Dividend Stocks:

Companies pay shareholders a portion of profits regularly (usually quarterly). You own the stock, money appears in your account automatically.

Top dividend payers for beginners:

- Coca-Cola (KO): ~3% dividend yield, 60+ years of increases

- Johnson & Johnson (JNJ): ~3% yield, dividend aristocrat

- Realty Income (O): ~5.5% yield, pays monthly

I hold $10,000 in dividend stocks generating roughly $350 annually. Not life-changing yet, but it’s completely passive and growing.

Dividend ETFs for diversification:

- SCHD (Schwab U.S. Dividend Equity ETF): ~3.5% yield

- VYM (Vanguard High Dividend Yield ETF): ~3% yield

- DGRO (iShares Core Dividend Growth ETF): ~2.5% yield + growth

REITs (Real Estate Investment Trusts):

REITs legally must distribute 90% of taxable income to shareholders. Translation: BIG dividends.

My favorite REITs:

- VNQ (Vanguard Real Estate ETF): Diversified, ~4% yield

- O (Realty Income): Monthly payments, ~5.5% yield

- STAG Industrial: Industrial properties, ~4% yield

I invested $5,000 in VNQ three years ago. It’s now worth $6,800 AND generates $270 annually in dividends. That’s passive income PLUS capital appreciation.

Index Funds with Dividend Focus:

Not every stock needs to pay dividends, but dividend-focused indexes provide regular income while still growing your principal.

Bond Income:

Bonds pay regular interest. They’re boring, stable, and perfect for passive income.

- BND (Total Bond Market): ~4% yield currently

- Treasury bonds: Government-backed, ultra-safe

- Municipal bonds: Tax-free income (great for high earners)

The Passive Income Snowball Effect:

Here’s where it gets REALLY cool. You reinvest dividends to buy more shares, which generate more dividends, which buy more shares. Compound growth on steroids.

Example of dividend reinvestment power:

| Years | Initial Investment | Value with Reinvested Dividends | Value without Reinvestment |

| 10 | $10,000 | $18,500 | $15,800 |

| 20 | $10,000 | $38,400 | $27,100 |

| 30 | $10,000 | $76,100 | $43,200 |

Same starting investment, but reinvesting dividends created an extra $32,900 over 30 years. That’s the power of passive income compounding.

My Passive Income Strategy:

Phase 1 (Current – Building):

- 70% growth index funds (VTI, VXUS)

- 20% dividend stocks/ETFs (SCHD, VYM)

- 10% REITs (VNQ, O)

Phase 2 (5-10 years – Transitioning):

- 50% growth index funds

- 40% dividend stocks/ETFs

- 10% bonds

Phase 3 (Financial Independence):

- 30% growth stocks

- 50% dividend stocks/REITs

- 20% bonds

The goal? Generate $4,000+ monthly in passive income within 15 years. Totally achievable with consistent investing and reinvestment.

Pro Tip: Enable automatic dividend reinvestment (DRIP) on all your accounts. Every dividend automatically buys more shares. You never touch the money, and your snowball grows faster.

12. Top Recommended Tools and Platforms for Beginners

You need the right tools to succeed. Here’s my definitive guide to platforms I actually use and recommend—not just random apps I Googled.

Robo-Advisors: Betterment, Wealthfront

Robo-advisors are perfect if you want completely hands-off investing. They build portfolios, rebalance automatically, and optimize taxes. You literally do nothing except add money.

Betterment:

What I love:

- No minimum investment (perfect for beginners)

- Automatic rebalancing and tax-loss harvesting

- Clean, simple interface

- Goal-based investing (retirement, house, vacation)

Costs: 0.25% annually ($25 per $10,000 invested)

Best for: Total beginners who want professional management without the effort.

I used Betterment for my first two years investing. It taught me portfolio construction while growing my money. No regrets.

Wealthfront:

What I love:

- $500 minimum (still very accessible)

- Sophisticated tax optimization

- Free financial planning tools

- Automatic rebalancing

Costs: 0.25% annually

Best for: Slightly more advanced beginners who want premium features.

Betterment vs Wealthfront comparison:

| Feature | Betterment | Wealthfront |

| Minimum | $0 | $500 |

| Fee | 0.25% | 0.25% |

| Tax-loss harvesting | Yes | Yes (more advanced) |

| Financial planning | Basic | Comprehensive |

| Best for | Absolute beginners | Tech-savvy investors |

Both are excellent. Pick based on your starting capital and desired features.

Apps for Beginners: Acorns, Robinhood, Sofi Invest

These apps make investing stupidly simple. Great for dipping your toes without commitment.

Acorns:

The concept: Rounds up purchases to the nearest dollar and invests the difference. Bought coffee for $3.50? Invests $0.50 automatically.

Why I recommend it:

- You invest without “feeling” it

- Perfect for people who “can’t afford” to invest

- Automatic diversification

- Genuinely painless

Costs: $3-$12/month (can eat into small balances)

Best for: Complete beginners with limited funds who need forced saving.

My sister used Acorns for a year, thought she couldn’t save. She accumulated $1,200 without even noticing. Sometimes you need to trick yourself into building wealth.

Robinhood:

Why it’s popular:

- Zero commissions

- Beautiful, intuitive interface

- Fractional shares (buy $5 of Amazon)

- Perfect for learning

Warning: The ease of trading can encourage bad behavior. Don’t day trade. Seriously.

Best for: Beginners who want to learn by doing with small amounts.

I use Robinhood for my 5% “fun money” allocation. I buy individual stocks I believe in, learn how markets work, and satisfy my investing curiosity without risking my serious portfolio.

Sofi Invest:

What makes it special:

- No fees on stocks or ETFs

- Automated investing option

- Great educational content

- Member benefits (career coaching, financial planning)

Best for: Millennials wanting an all-in-one financial platform.

Best Platforms for Long-Term Growth: Vanguard, Fidelity, Schwab

These are the big three. Serious investors eventually end up here. They’re not flashy, but they’re POWERFUL.

Vanguard:

The legend: Created the first index fund. Investor-owned (not profit-driven). Lowest fees in the industry.

Why I use it:

- Rock-bottom fees (VTSAX expense ratio: 0.04%)

- Incredible fund selection

- Long-term investor focus

- No gimmicks, just results

Con: Website and app feel outdated

Best for: Long-term buy-and-hold investors who prioritize low costs.

My Roth IRA is at Vanguard. I don’t care about fancy interfaces—I care about keeping every possible penny of my returns.

Fidelity:

The all-rounder: Great platform, great funds, great tools. Does everything well.

Why I recommend it:

- ZERO expense ratio funds (FZROX, FNILX)

- Excellent research tools

- Better customer service than Vanguard

- Modern, user-friendly platform

Best for: Beginners who want powerful tools without complexity.

Fidelity is my taxable brokerage account. The ZERO fee funds are unbeatable, and their customer service actually answers phones quickly.

Charles Schwab:

The innovator: Best-in-class platform, incredible customer service, powerful tools.

Why it’s great:

- No account minimums

- Exceptional research and education

- Schwab Intelligent Portfolios (free robo-advisor)

- Over 300 branches for in-person help

Best for: Investors who want premium service without premium fees.

The Big Three Comparison:

| Feature | Vanguard | Fidelity | Schwab |

| Account minimum | $0-$1,000 | $0 | $0 |

| Fund selection | Excellent | Excellent | Excellent |

| Platform quality | Dated | Modern | Modern |

| Customer service | Average | Great | Excellent |

| Zero-fee funds | No | Yes | No |

| Best feature | Lowest overall costs | ZERO funds | Premium service |

My honest recommendation: Start with Fidelity. Once you hit $10,000+, open a Vanguard Roth IRA for tax-free growth. You can’t go wrong with any of these three.

Pro Tip: Don’t overthink this decision. The platform matters WAY less than actually investing consistently. Pick one, open the account TODAY, and start building wealth. You can always transfer accounts later if needed.

The tools are here. The knowledge is here. The only thing missing? YOUR action. Stop researching and start investing.

Conclusion: Your Path to Financial Freedom Starts Today

We’ve covered A LOT in this guide. From understanding what financial freedom actually means to choosing specific funds, from avoiding scams to building passive income streams. But here’s what I need you to understand: All this knowledge means NOTHING without action.

I’ve met countless people who’ve read every investing book, watched hundreds of YouTube videos, and can quote Warren Buffett in their sleep. You know what they have in common? They’re still broke because they never actually invested.

Don’t be that person.

Here’s the beautiful truth about investing: You don’t need to be perfect. You don’t need a finance degree. You don’t need $10,000 sitting in your bank account. You just need to START.

Remember that compound interest chart we looked at earlier? The one showing how $500 monthly grows to over $745,000 in 30 years? That doesn’t happen by reading articles. It happens by DOING something with the information.

Your action plan for this week—yes, THIS WEEK:

Day 1-2: Choose your platform (Fidelity, Vanguard, or Schwab for serious investing; Acorns or Robinhood for starting small)

Day 3: Open your account (takes 15 minutes, I promise)

Day 4: Link your bank account and transfer your first investment—even if it’s just $50

Day 5: Buy your first investment (VTI, FZROX, or a target-date fund—keep it simple)

Day 6: Set up automatic monthly contributions (this is THE most important step)

Day 7: Close your investing apps and GO LIVE YOUR LIFE

That’s it. Seven days to completely change your financial trajectory. Seven days to start building the wealth that’ll give you OPTIONS, FREEDOM, and SECURITY.

I started with $50 eight years ago. I felt ridiculous investing such a small amount. Today, that disciplined approach has built a six-figure portfolio that generates passive income while I sleep. I’m not special. I’m not lucky. I just STARTED and stayed consistent.

The worst investment you can make is doing nothing.

While you’re waiting for the “perfect time” or the “right amount,” inflation is eating your savings and time is ticking away. Every month you delay costs you thousands in future gains.

Financial freedom isn’t a destination you arrive at one day. It’s a journey you start TODAY. It’s the small, consistent actions—$100 here, $200 there—that compound into life-changing wealth over time.

You’ve got the knowledge. You’ve got the roadmap. You’ve got the exact tools and platforms to use. The ONLY question remaining is: Will you take action?

Your future self is watching. What decision are you making today? The decision to stay comfortable and broke, or the decision to feel uncomfortable for a moment and become wealthy?

I know what I chose. And I’m living proof it works.

Start investing today—your future self will thank you.

Now stop reading and GO OPEN THAT ACCOUNT. Seriously. Right now. I’ll wait.

FAQs: Investing for Financial Freedom

Got questions? Of course you do. Let me answer the ones I hear constantly from beginners just like you.

What is the first step to start investing?

The absolute FIRST step isn’t opening an account—it’s getting your financial house in order. Pay off high-interest debt (anything above 7%), build a small emergency fund of at least $1,000, and understand your monthly budget.

Once that’s handled, here’s your literal step-by-step:

- Choose a platform (I recommend Fidelity for beginners—zero-fee funds and great tools)

- Open a Roth IRA if you’re eligible (tax-free growth forever)

- Start with $50-100 if that’s what you have

- Invest in a simple index fund like FZROX or VTI

- Set up automatic monthly contributions

- Ignore the account for at least a month

The hardest part is clicking “submit” on that first investment. After that? It gets easier every single time. I remember my hands literally shaking when I invested my first $50. Now it’s completely automatic and I don’t even think about it.

Pro tip: Don’t wait until you “understand everything.” You’ll learn more by DOING than by reading another ten articles. Start small, learn as you go, and increase your knowledge alongside your portfolio.

How long does it take to achieve financial freedom?

The honest answer? It depends on three things: how much you invest, what returns you earn, and what your expenses are.

But let me give you real numbers:

Scenario 1: Aggressive saver

- Invest $1,000/month at 8% returns

- Annual expenses: $40,000

- Financial freedom in: 18-20 years

Scenario 2: Moderate investor

- Invest $500/month at 8% returns

- Annual expenses: $30,000

- Financial freedom in: 25-28 years

Scenario 3: Starting small

- Invest $200/month at 8% returns

- Annual expenses: $25,000

- Financial freedom in: 35-40 years

Notice the pattern? The MORE you invest and the LESS you spend, the faster you reach freedom. It’s math, not magic.

I’m currently on a 15-year track to financial independence because I invest aggressively (about 40% of my income) and keep my expenses reasonable. Some people do it in 10 years. Others take 30. There’s no “right” timeline—only YOUR timeline.

The real question isn’t “how long will it take?” It’s “when do I START?” Because every month you delay adds 2-3 months to your timeline due to lost compound growth.

Should I invest in stocks or mutual funds?

This question shows a common misconception, so let me clear it up: Mutual funds (specifically index funds) contain stocks. You’re not choosing between them—you’re choosing HOW you invest in stocks.

Here’s the real comparison:

Individual stocks:

- Higher risk (one company can tank)

- Requires research and monitoring

- Can have big wins OR big losses

- Best for: 5-10% of your portfolio once you’re experienced

Mutual funds/Index funds:

- Lower risk (hundreds of companies)

- Minimal research needed

- Steady, reliable returns

- Best for: 90-95% of your portfolio, especially as a beginner

My recommendation? Start with index funds, period. Put 100% of your money in something like VTI (Total Stock Market) or FZROX (Fidelity Zero Total Market). These funds own thousands of companies, so you’re betting on the entire economy growing—not picking individual winners.

Once you’ve got $10,000+ invested and understand the market better, THEN consider putting 5% in individual stocks if you want. But honestly? Most people never need to buy individual stocks. Index funds outperform 90% of professional stock pickers over time.

I keep 95% in index funds and 5% in individual stocks for fun. That 5% satisfies my curiosity and teaches me about markets without risking my financial future.

How do I open an investment account in the USA?

Opening an investment account is EASIER than opening a bank account. I’m serious. Here’s exactly how to do it:

For a standard brokerage account:

- Go to Fidelity.com, Vanguard.com, or Schwab.com

- Click “Open an Account”

- Choose “Individual Brokerage Account” (or Roth IRA if eligible)

- Enter your personal info (name, address, SSN, date of birth)

- Answer a few questions about your financial situation

- Link your bank account

- Done! Takes 10-15 minutes max

Documents you’ll need:

- Social Security Number or Tax ID

- Driver’s license or government ID

- Bank account for transfers

- Employment information

That’s literally it. No complicated paperwork, no office visits, no confusion. The platforms walk you through everything step-by-step.

For a Roth IRA (highly recommended):

Same exact process, but choose “Roth IRA” instead of brokerage account. The platform will verify you meet income requirements (under $161,000 for singles, $240,000 for married couples in 2025).

I’ve opened accounts with Fidelity, Vanguard, and Schwab. Every single time took under 20 minutes. The platforms are designed for beginners—they WANT your money, so they make it ridiculously easy.

Pro tip: Have your first deposit amount ready. Many platforms let you transfer immediately, so you can be invested within hours of opening your account.

How can I reduce risk as a beginner investor?

Risk management is EVERYTHING, especially when you’re starting out. Here’s exactly how to protect yourself while still growing wealth:

Strategy #1: Diversify relentlessly

Never put more than 5% of your portfolio in any single stock. Instead, use index funds that own hundreds or thousands of companies. If one fails, you barely notice. This is THE most important risk reducer.

Strategy #2: Match your timeline to your investments

Need money in 2 years? Don’t invest it—save it in a high-yield savings account. Money you won’t need for 10+ years? Invest aggressively in stocks. This prevents forced selling during downturns.

Strategy #3: Use the age-based allocation rule

Subtract your age from 110. That’s your stock percentage. The rest goes in bonds.

- Age 25: 85% stocks, 15% bonds

- Age 40: 70% stocks, 30% bonds

- Age 60: 50% stocks, 50% bonds

Strategy #4: Dollar-cost average

Invest the same amount monthly regardless of market conditions. This averages out your purchase price and removes the temptation to time the market. I invest $800 every single month on the 1st—whether the market is up, down, or sideways.

Strategy #5: Keep emotions in check

The biggest risk isn’t market crashes—it’s YOU panicking and selling. During the 2020 crash, people who held their investments recovered within months. People who sold locked in permanent losses.

Set up automatic investments, check your portfolio monthly (not daily), and remind yourself that temporary drops are NORMAL and expected.

Strategy #6: Build an emergency fund first

Keep 3-6 months of expenses in a savings account BEFORE investing seriously. This prevents you from selling investments when life happens (car breaks, job loss, medical bills).

I sleep well at night because I’m diversified across thousands of companies, I invest consistently regardless of market conditions, and I have 6 months of expenses sitting safely in cash. Risk is managed, not eliminated—and that’s exactly how it should be.

Now I want to hear from YOU.

What’s been holding you back from investing? Is it fear? Lack of knowledge? Not enough money? Or have you already started your investing journey—and if so, what’s been your biggest lesson?

Drop your thoughts, questions, or experiences in the comments below. I read every single one, and I love hearing about your financial journeys. Let’s learn from each other and build wealth together.

Your turn—comment below and let’s talk!