How to Build a Financial Independence Plan: A Step-by-Step Guide to Passive Income, Personal Finance & Wealth Management

Let me ask you something: what if the secret to financial independence isn’t really about earning MORE money, but about managing the money you already have with INTENTION?

Think about that for a second. Most people are chasing bigger paychecks while their spending runs wild, their debt piles up, and their future retirement stays a foggy dream. But here’s the truth, building a solid financial independence plan doesn’t start with a six-figure salary. It starts with a decision.

You have the power to take control of your money, and your life, starting TODAY.

In this guide, I’m going to walk you through everything you need to know: budgeting, saving, smart investing, passive income ideas, debt reduction, tax planning, and retirement. Step by step. No jargon. No fluff. Just a clear, practical roadmap that actually works.

Whether you’re in your 20s just starting out, your 30s trying to reset, or your 40s playing catch-up, this is YOUR guide to personal finance and wealth management that leads somewhere real.

Let’s build that plan.

1. What Is Financial Independence?

Let’s get one thing clear right away — financial independence is NOT the same as being rich.

I know, I know. A lot of people confuse the two. But here’s the real definition: financial independence means having enough money working FOR you — through savings, investments, and passive income streams — that you no longer HAVE to work to cover your living expenses. Your money earns money. Your time becomes yours again.

That’s the dream, right?

Being wealthy, on the other hand, is about net worth on paper. You can have a millionaire neighbor driving a luxury car who is one missed paycheck away from financial collapse — and a school teacher quietly living on 60% of their income, investing the rest, who retires at 52 with zero stress. Wealth is a number. Financial independence is a lifestyle and a system.

The Income vs. Savings Rate Equation

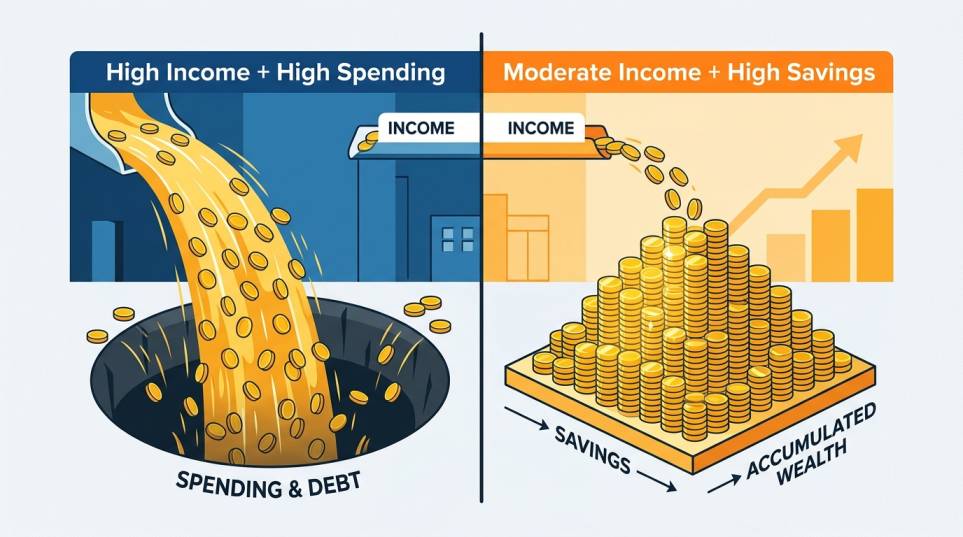

Here’s something most financial articles won’t tell you straight: your savings rate matters MORE than your income level. Yes, you read that right.

Let me break it down:

If you earn $5,000 a month but spend $4,800, your savings rate is just 4%. You’re essentially running on a financial treadmill — moving fast but going nowhere.

But if you earn $3,500 a month and spend only $2,100, your savings rate is 40%. THAT person is on the road to financial independence — regardless of the smaller paycheck.

The formula is simple:

Savings Rate = (Income – Expenses) ÷ Income × 100

The higher your savings rate, the fewer years you need to work before money starts working FOR you. Check out this quick reference:

| Savings Rate | Approximate Years to Financial Independence |

| 10% | ~37 years |

| 20% | ~30 years |

| 30% | ~22 years |

| 40% | ~16 years |

| 50% | ~12 years |

| 60%+ | ~8 years or less |

Based on the 4% safe withdrawal rule, commonly used in FIRE (Financial Independence, Retire Early) planning.

Why does financial independence matter so much? Because without it, you’re always one job loss, one medical emergency, or one economic downturn away from a crisis. Financial independence gives you OPTIONS — the freedom to choose where you work, how you live, and what you build.

That’s the version of freedom we’re building toward in this guide. And it starts with something deceptively simple: setting goals.

2. Set Clear Financial Goals

You wouldn’t get in a car and start driving without knowing where you’re headed. So why do most people manage money without a single clear destination?

Setting financial goals is the foundation of any serious financial independence plan. Without them, budgeting feels like punishment, saving feels pointless, and investing feels like gambling. But with them? Every dollar you manage has a JOB to do.

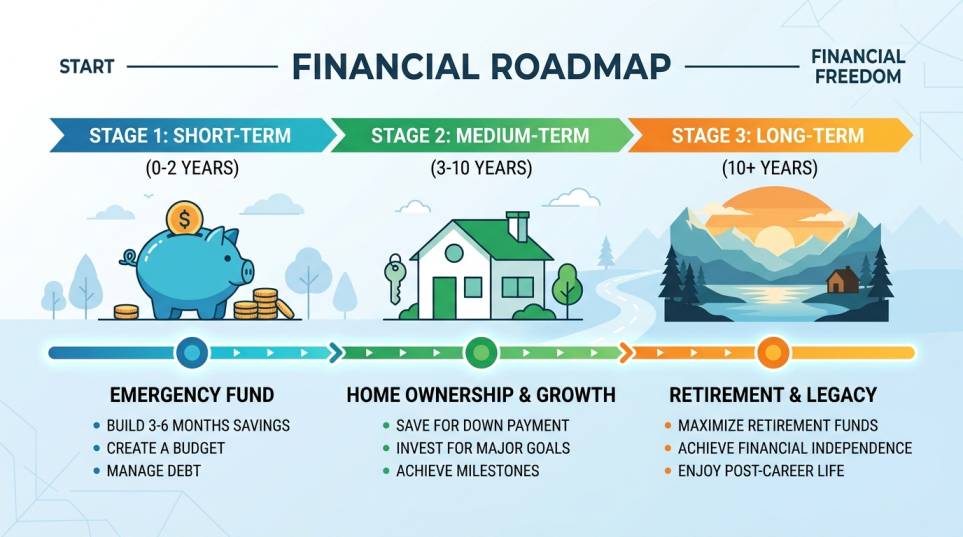

Here’s how to break your financial goals into three horizons — and make each one stick.

Short-Term Financial Goals (0–2 Years)

These are the wins you want to achieve RIGHT NOW. They’re the building blocks — and honestly, the most motivating, because you can see results fast.

Examples of smart short-term financial goals:

- Pay off one credit card completely

- Save a $1,000 starter emergency fund within 90 days

- Cut your monthly spending by 15%

- Set up automatic savings transfers

- Start tracking every dollar you spend

The key here is specificity. Don’t say “I want to save more money.” Say: “I will save $300 every month for the next 12 months by reducing dining out and cancelling two unused subscriptions.” That’s a goal you can actually measure — and achieve.

Medium-Term Financial Goals (2–5 Years)

These are the goals that require sustained effort and smart strategy. They’re bigger, yes — but completely achievable when you’ve nailed the short-term habits.

Examples:

- Build a 6-month emergency fund ($15,000–$30,000 depending on lifestyle)

- Pay off all consumer debt (car loans, credit cards, student loans)

- Save for a home down payment

- Start a side income or passive income stream

- Max out a Roth IRA or 401(k) contribution for the year

Long-Term Financial Goals (5+ Years)

This is where the BIG picture lives. These goals define what financial independence actually looks like FOR YOU.

Examples:

- Retire early (or at least retire on YOUR terms)

- Build a real estate or dividend investment portfolio

- Generate $3,000–$5,000/month in completely passive income

- Achieve a net worth of $1M or more

- Leave a financial legacy for your family

How to Make Financial Goals Measurable and Realistic

Good financial goal-setting follows the SMART framework — and I’m going to adapt it specifically for money:

| SMART Criteria | Applied to Finance |

| Specific | “Save $10,000 for a home down payment” not “save money” |

| Measurable | Track monthly progress — are you on pace? |

| Achievable | Set stretch goals, but grounded in your actual income |

| Relevant | Does this goal align with your bigger financial vision? |

| Time-Bound | “By December 31st” beats “someday” every single time |

One tool I love for this is Quicken Simplifi — it lets you set financial goals by category and tracks your real-time progress automatically. No guessing whether you’re on track. You just log in and you KNOW.

Pro Tip: Write your financial goals down physically — not just in an app. Research shows that people who write their goals down are 42% more likely to achieve them. Keep that list somewhere you’ll see it every day.

Now that your goals are locked in, we need to build the engine that funds them. That’s your budget — and your safety net.

3. Build a Budget and Emergency Fund

Okay, real talk: “budgeting” gets a bad reputation. People hear the word and immediately think restrictions, sacrifice, and spreadsheets from 1997. But here’s what I’ve learned — a budget isn’t a cage. It’s a PLAN. And when your money has a plan, your goals stop feeling impossible.

Let’s build yours from scratch.

Step 1: Track Your Income and Expenses

Before you can control your money, you need to SEE it. All of it.

For one full month, write down (or record in an app) every single dollar that comes in AND goes out. I mean every coffee. Every impulse Amazon order. Every subscription you forgot you had. You’ll be surprised — most people discover they’re “leaking” $300–$600/month on spending they don’t even remember.

Categorize your spending into three buckets:

- Fixed expenses — rent/mortgage, car payments, insurance, utilities

- Variable necessities — groceries, gas, medical

- Discretionary spending — dining out, entertainment, shopping, subscriptions

This awareness alone changes behavior. You can’t fix what you can’t see.

Step 2: Choose a Budgeting Method That Works for YOU

There’s no one-size-fits-all budgeting method — and that’s actually GREAT news, because you get to pick the one that fits your personality and lifestyle.

Here are the three most effective ones:

The 50/30/20 Rule

| Category | Percentage | What It Covers |

| Needs | 50% | Housing, utilities, groceries, transport |

| Wants | 30% | Dining, entertainment, travel, hobbies |

| Savings/Debt | 20% | Emergency fund, investments, debt repayment |

Best for: Beginners who want simplicity without obsessing over every line item.

Zero-Based Budgeting

Every dollar gets assigned a job — income minus all expenses and savings equals ZERO. You’re not spending zero; you’re allocating every dollar on purpose.

Best for: People serious about aggressive saving or debt payoff who want full control.

The Pay-Yourself-First Method

Transfer your savings automatically the moment your paycheck hits — BEFORE you pay anything else. Then live on what’s left.

Best for: People who find budgeting overwhelming but want to build wealth passively without thinking too hard about it.

Pro Tip: Combine Pay-Yourself-First with the 50/30/20 Rule for maximum impact. Automate your 20% savings on payday, then split the remaining 80% using the 50/30 model. Simple, powerful, and nearly effortless once it’s set up.

Step 3: Cut Unnecessary Spending (Without Feeling Miserable)

Here’s the deal — you don’t need to deprive yourself. You just need to audit your spending with fresh eyes.

Start with the “Cancel and Review” audit:

- Subscriptions: List every recurring payment. Cancel anything you haven’t used in 30 days

- Dining out: Try cutting restaurant spending by just 30% — it often saves $100–$200/month

- Utilities: Call your providers and ask for a loyalty discount or better rate. It works more often than you’d think

- Insurance: Get competing quotes annually — you could save $500–$1,500/year just by switching

- Grocery shopping: Meal plan weekly and use cashback apps like Ibotta or Rakuten

Small cuts, stacked consistently, add up to SERIOUS money over 12 months. Don’t underestimate them.

Step 4: Build Your Emergency Fund

This is non-negotiable. Before you invest a single dollar, before you open a brokerage account, before ANYTHING — you need an emergency fund. Full stop.

Here’s why: life WILL surprise you. A car repair. A medical bill. A sudden job loss. Without a financial cushion, you either go into debt or derail your entire financial plan. With one? You handle the emergency and move on without missing a beat.

How much do you need?

| Life Situation | Recommended Emergency Fund |

| Single, stable job | 3–4 months of expenses |

| Dual income household | 3 months of expenses |

| Single income family | 6 months of expenses |

| Self-employed/Freelancer | 9–12 months of expenses |

Where should you keep it? NOT in your checking account where it’s too easy to spend. Open a high-yield savings account (HYSA) — something like Marcus by Goldman Sachs or Ally Bank — where your money earns 4–5% interest while it waits. It’s safe, it’s accessible, and it’s growing.

Best Budgeting Apps and Budget Planner Tools in 2026

You don’t have to do this manually. Here are the best tools available right now:

| Tool | Best For | Cost |

| YNAB (You Need a Budget) | Zero-based budgeting, serious savers | $14.99/month |

| Quicken Simplifi | Goal tracking, automated insights | $3.99/month |

| Monarch Money | Couples and shared finances | $14.99/month |

| Copilot | Apple users who want beautiful UX | $13/month |

| Empower (Personal Capital) | Free net worth + investment tracking | Free |

| EveryDollar | Dave Ramsey fans, simple zero-based | Free / $17.99/month Premium |

My personal recommendation? Start with YNAB if you’re serious about paying off debt or building savings aggressively. It’s not just a budgeting app — it’s a financial mindset shift in app form. Thousands of users report saving an average of $600 in their first month alone.

Pro Tip: Don’t wait for the “perfect time” to start budgeting. Start TODAY with whatever you have. Open a free account on Empower to see your full financial picture in under 10 minutes — net worth, spending, and savings all in one dashboard. That clarity alone can be life-changing.

Your budget and emergency fund are now the launchpad. Everything else — investing, passive income, debt payoff — builds on THIS foundation. Next, we go deeper into the engine of wealth building: getting out of debt and investing your money to grow.

4. Reduce Debt Strategically

Debt is the single biggest roadblock standing between you and financial independence. I’m not being dramatic — it’s math. Every dollar you send to a lender in interest is a dollar that isn’t building YOUR future. And until you deal with it intentionally, it will quietly drain every financial plan you try to build.

The good news? You CAN get out of debt. Millions of people have done it — on average incomes, with average lives, and zero financial superpowers. You just need a strategy.

Why Debt Management Matters for Financial Independence

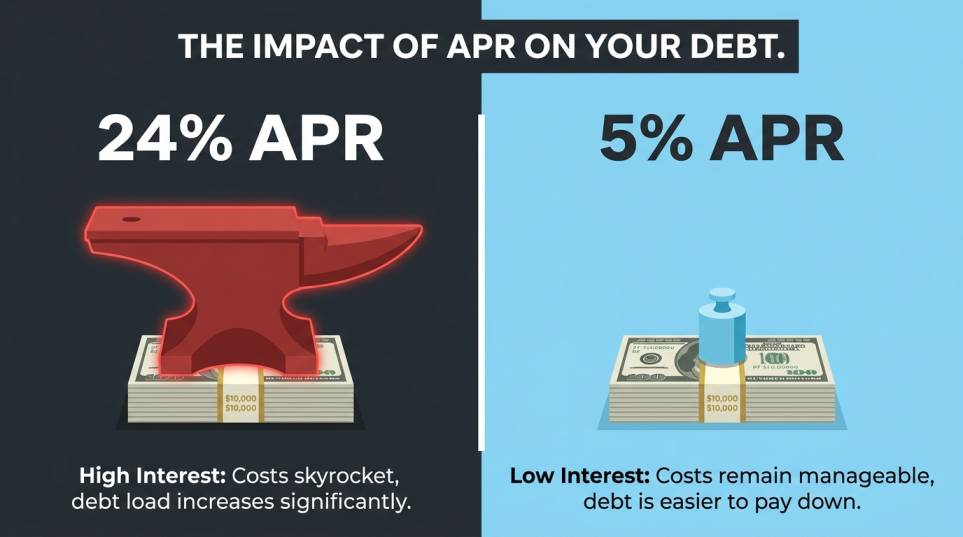

Let’s be blunt: you cannot reach financial independence while carrying high-interest debt. A credit card charging you 22% interest is essentially a -22% investment return. No stock market, no rental property, no side hustle can reliably beat that number over time.

Effective debt management isn’t just about getting a weight off your chest — though that feeling is INCREDIBLE. It’s about redirecting that monthly cash flow toward wealth-building instead of wealth-draining.

Here’s what paying off debt actually unlocks:

- More monthly cash flow for investing and saving

- A dramatically improved credit score (which lowers future borrowing costs)

- Lower financial stress — which, by the way, has real health benefits

- The mental freedom to take smart financial risks like starting a business or investing aggressively

High-Interest Debt First — Always

Not all debt is created equal. A 3.5% mortgage? That’s manageable. A 24% APR credit card balance? That’s a financial emergency wearing a plastic card.

Rank your debts by interest rate, highest to lowest. The top of that list gets your most aggressive repayment energy. This is just common sense financial strategy — and it WORKS.

Debt Snowball vs. Debt Avalanche: Which Should You Choose?

These are the two most popular and proven methods for paying off debt. Here’s how they compare:

| Strategy | How It Works | Best For | Speed to Payoff |

| Debt Snowball | Pay minimums on all debts; attack the SMALLEST balance first | People who need motivational wins to stay consistent | Slower mathematically |

| Debt Avalanche | Pay minimums on all; attack the HIGHEST interest rate first | People who are disciplined and want to save the most money | Faster and cheaper overall |

Debt Snowball — popularized by Dave Ramsey — works brilliantly for people who need psychological momentum. Knock out that small $800 store card first, and suddenly you FEEL like you’re winning. That energy keeps you going.

Debt Avalanche — the math-first approach — saves you more money in interest over time. If you owe $15,000 on a 24% APR card and $500 on a 12% card, the avalanche says: ignore the small balance, attack the expensive one.

My honest take? If you’re emotionally struggling with debt, start with the snowball. The psychological wins matter MORE than perfect math when you’re fighting to stay motivated. Once you build momentum, you can always switch to the avalanche method.

Pro Tip: Use a free tool like Undebt.it or the debt payoff planner in YNAB to map your exact payoff date under both strategies. Seeing a specific month and year when you’ll be debt-free is POWERFUL motivation.

When to Pause Investing and Focus on Debt

This is a question I get all the time: “Should I invest while paying off debt?”

Here’s the honest answer — it depends on the interest rate:

| Debt Interest Rate | Recommended Approach |

| Below 5% (mortgage, some student loans) | Continue investing; the market likely outperforms this rate long-term |

| 5–8% (car loans, some personal loans) | Split your extra cash — half to debt, half to investing |

| Above 8% (credit cards, payday loans) | PAUSE investing (except 401k employer match); attack debt aggressively |

The one exception to pausing investing? Always capture your employer’s 401(k) match. That’s an instant 50–100% return on your money — no investment on earth beats that. Grab the match, then throw everything else at your high-interest debt.

Once the debt is cleared, you redirect every dollar of those former debt payments straight into your investment accounts. That’s when your financial independence journey truly accelerates.

5. Start Investing for Long-Term Growth

Now HERE is where things get exciting.

Once your emergency fund is solid and your high-interest debt is under control, investing becomes your most powerful tool for building wealth. Not a savings account. Not a CD. INVESTING — in assets that grow, compound, and multiply over decades.

And before you say “but I don’t know enough to invest” — let me stop you right there. Investing for beginners has never been more accessible than it is today. You don’t need a financial advisor with a mahogany desk. You need a smartphone, a brokerage account, and the willingness to start.

Why Investing Is Non-Negotiable

Keeping your money in a savings account feels safe. But here’s the brutal truth: inflation is quietly eating it alive.

If inflation runs at 3% annually and your savings account earns 0.5%, you’re LOSING purchasing power every single year you don’t invest. Over 20–30 years, the cost of inaction is staggering.

But the stock market, historically, has returned an average of 7–10% annually (adjusted for inflation). That means money invested consistently over time doesn’t just grow — it COMPOUNDS.

The power of compound growth — $500/month invested:

| Years Invested | At 7% Average Return | At 10% Average Return |

| 10 years | ~$86,000 | ~$95,000 |

| 20 years | ~$245,000 | ~$305,000 |

| 30 years | ~$567,000 | ~$790,000 |

That’s the same $500/month. The only variable is time. THIS is why starting early — even imperfectly — beats waiting until you feel “ready.”

How to Start Investing: Beginner-Friendly Options

Here’s a clean breakdown of beginner-friendly investment vehicles, so you know exactly how to start investing without confusion:

How so start investing

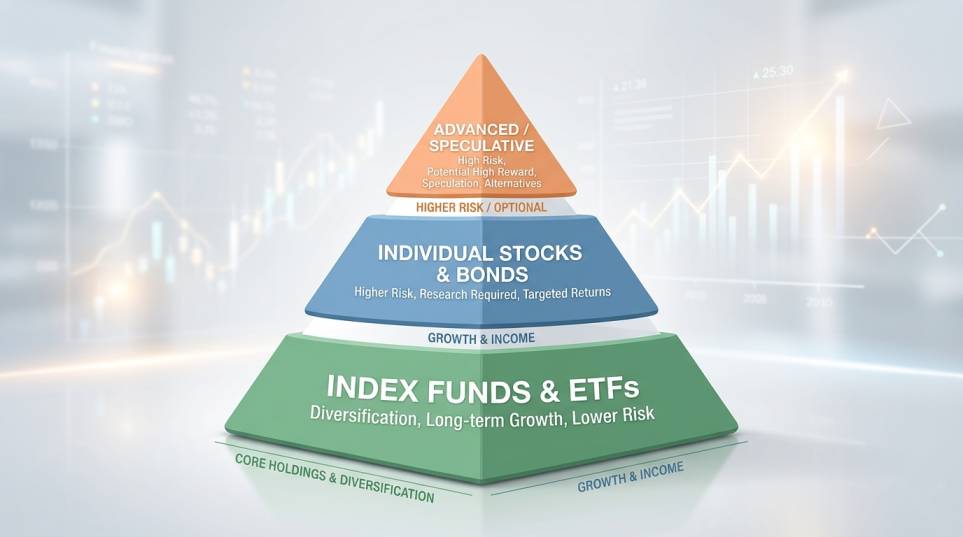

1. Index Funds

These track a market index — like the S&P 500 — and give you instant diversification across hundreds of companies. Low fees. Historically strong returns. Warren Buffett himself recommends index funds for most everyday investors. Start here.

2. ETFs (Exchange-Traded Funds)

Think of ETFs like index funds you can buy and sell like a stock. A solid ETF investment strategy for beginners: buy a total market ETF (like VTI) and a total international ETF (like VXUS), set up automatic monthly contributions, and leave it alone. That’s genuinely it.

3. Mutual Funds

Pooled investments managed by professionals. Higher fees than ETFs typically, but some actively managed funds deliver strong long-term performance. Good for retirement accounts where you want a hands-off approach.

4. Individual Stocks

Higher risk, higher potential reward. Don’t start here as a beginner. If you want individual stocks eventually, limit them to 10–15% of your portfolio maximum. Keep the core in diversified funds.

5. Retirement Accounts (401k / IRA / Roth IRA)

These are the tax-advantaged accounts that SUPERCHARGE your investment returns. This is where most of your investing should live:

| Account | Tax Treatment | 2025 Contribution Limit | Best For |

| 401(k) | Pre-tax contributions, taxed on withdrawal | $23,000 ($30,500 if 50+) | Employer-sponsored workplace savings |

| Traditional IRA | Pre-tax (if eligible), taxed on withdrawal | $7,000 ($8,000 if 50+) | Those expecting lower tax rate in retirement |

| Roth IRA | After-tax contributions, tax-FREE growth | $7,000 ($8,000 if 50+) | Younger investors expecting higher future income |

My personal recommendation: if you’re under 40, a Roth IRA is gold. You pay taxes now and NEVER pay taxes on the growth again. Over 30–40 years of compounding, that tax-free growth is worth an enormous amount.

Diversification: Don’t Put All Your Eggs in One Basket

This is the cardinal rule of investment strategies — spread your risk.

A well-diversified beginner portfolio might look something like this:

- 60% — US Total Market Index Fund (e.g., VTI or FSKAX)

- 20% — International Index Fund (e.g., VXUS or FZILX)

- 15% — Bond Index Fund (e.g., BND) — adds stability

- 5% — REITs or alternatives — real estate exposure without buying property

Adjust the ratios based on your age and risk tolerance. Younger investors can afford more stocks (higher risk, higher reward). As you approach retirement, shift gradually toward bonds and income-producing assets.

Best Platforms for Beginner Investors

| Platform | Best Feature | Minimum to Start |

| Fidelity | Zero-fee index funds, excellent retirement tools | $0 |

| Vanguard | The OG of low-cost investing | $1 (ETFs) |

| Charles Schwab | Great research tools and fractional shares | $0 |

| M1 Finance | Automated “pie” investing — set and forget | $100 |

| Betterment | Full robo-advisor, handles everything for you | $0 |

Pro Tip: Automate your investments the same way you automated your savings. Set a recurring monthly transfer into your brokerage or Roth IRA on payday. You’ll never miss the money — and future you will be VERY grateful.

6. Create Passive Income Streams

Here’s a mindset shift that changes everything: what if your money worked while you slept?

That’s exactly what passive income does. It decouples your earnings from your hours — which is the fundamental difference between people who achieve financial independence and people who stay stuck trading time for money their entire working lives.

Let me be real with you though: most “passive” income requires upfront work or capital. But once you build it? The ongoing effort is minimal — and the financial impact is MASSIVE.

What Is Passive Income?

Passive income is money earned with little to no active daily effort on your part — generated from assets you’ve built, bought, or automated. It’s not “do nothing, get rich” (that’s a scam). It’s “work hard once, earn repeatedly.”

The goal is simple: build enough passive income streams to cover your monthly living expenses. When your passive income exceeds your expenses — you’ve reached financial independence.

The Best Passive Income Ideas in 2026

Here’s a breakdown of proven passive income ideas, organized by how much money and effort they require to start:

Low Capital Required (Start with Under $1,000)

- Dividend investing — Buy dividend-paying ETFs like SCHD or VYM. As your portfolio grows, these pay you quarterly income just for holding shares

- High-yield savings accounts — Not glamorous, but a $30,000 emergency fund at 5% APY earns $1,500/year passively

- Digital products — Create an ebook, Notion template, or Canva template once, sell it forever on platforms like Gumroad or Etsy

- Print-on-demand — Design t-shirts, mugs, or art prints. Platforms like Printful handle everything. You earn royalties on each sale

- YouTube AdSense — Build a channel (like Wisdom Tales of Africa, for example). Once you hit monetization thresholds, videos earn money indefinitely

Medium Capital Required ($1,000–$10,000)

- Peer-to-peer lending — Platforms like Prosper allow you to earn interest by lending to others

- REITs (Real Estate Investment Trusts) — Invest in real estate WITHOUT buying property. REITs are traded like stocks and pay regular dividends

- Online courses — Record a course on a skill you know well. Platforms like Teachable or Udemy sell it for you 24/7

- Affiliate marketing through a blog or YouTube — Recommend products you genuinely use. Earn a commission every time someone buys through your link

Higher Capital Required ($10,000+)

- Rental properties — Classic wealth-builder. Requires capital and management, but monthly rental income can be life-changing

- Dividend stock portfolio — Build a portfolio large enough that dividends alone cover monthly expenses. $500,000 at a 4% dividend yield = $20,000/year passively

- Buy an existing online business — Platforms like Flippa let you purchase established blogs, e-commerce stores, or apps already generating revenue

Side Hustles That Can Grow Into Income Streams

Some of the best passive income streams start as active side hustles — and gradually become self-sustaining with the right systems. Here’s how that transition works:

| Side Hustle | Active Phase | How It Becomes Passive |

| Blogging / SEO content | Writing articles consistently | Articles rank on Google and earn ad/affiliate revenue forever |

| YouTube channel | Creating and uploading videos | Old videos continue generating AdSense income indefinitely |

| Selling digital products | Creating templates, ebooks, courses | Automated sales funnels sell products while you sleep |

| Dropshipping store | Setting up products and marketing | Automated order fulfillment with minimal daily management |

| Rental property | Finding, financing, preparing property | Monthly rent arrives with a good property manager in place |

The key takeaway: most passive income starts active. You put in the work upfront — then you build the systems that run without you.

Why Multiple Income Streams Are Essential

Relying on a single paycheck is a financial vulnerability. One layoff, one health crisis, one economic downturn — and your entire financial plan collapses.

Multiple income streams give you something priceless: resilience. When one stream slows down, the others keep flowing. The wealthiest people I’ve studied don’t have one source of income. They have five, six, sometimes ten.

You don’t need to build them all at once. Start with one. Master it. Then add another. Over three to five years, you can realistically build a diversified income ecosystem that no single employer, client, or market can take down.

Pro Tip: Start your first passive income stream in an area where you already have knowledge or an audience. If you know Excel, sell spreadsheet templates on Etsy. If you love personal finance, start a blog with affiliate links. The best passive income stream is the one you’ll actually build — and the best starting point is always what you already know.

With your debt shrinking, your investments growing, and passive income beginning to flow, you’re now building on a genuinely solid financial foundation. Next, we tackle two of the most overlooked yet powerful tools in your financial independence toolkit: tax planning and retirement strategy.

7. Plan for Taxes and Retirement

Let me be honest with you — tax planning and retirement planning are the two areas where most people either procrastinate completely or make expensive mistakes they don’t even realize until it’s too late.

And that’s a shame. Because done RIGHT, these two pillars can shave YEARS off your financial independence timeline and save you tens of thousands of dollars in the process.

Let’s fix that — starting now.

Why Tax Planning Matters More Than You Think

Here’s something your paycheck doesn’t make obvious: taxes are likely your single largest lifetime expense. More than your mortgage. Your car. More than everything in your grocery cart combined — over a lifetime.

The average American pays between 25–35% of their income in combined federal, state, and payroll taxes. That’s a massive chunk of your earning power leaving every single year. And yet most people do absolutely NOTHING to legally minimize it.

Tax planning isn’t about cheating the system. It’s about understanding the rules well enough to use every legal advantage available to you. The IRS literally wrote tax breaks into the law — for retirement savers, investors, homeowners, and business owners. Your job is to USE them.

Here’s how taxes directly affect your financial independence timeline:

| Tax Strategy | Potential Annual Savings | Impact Over 20 Years |

| Max out 401(k) pre-tax contributions | $5,000–$8,000/year in taxes | $100,000–$160,000+ saved |

| Contribute to a Roth IRA | Tax-free growth on decades of compounding | $200,000–$500,000+ in tax-free wealth |

| Tax-loss harvesting on investments | $500–$3,000/year depending on portfolio | Significant compounding benefit |

| Deduct home office / business expenses | $1,000–$5,000+/year | Substantial reduction in taxable income |

| Hold investments 12+ months (long-term capital gains) | 15% vs. 37% tax rate on gains | Massive difference on large investment exits |

The bottom line: a dollar saved in taxes is a dollar that stays in YOUR portfolio, compounding for YOUR future.

Retirement Accounts: The Ultimate Tax Advantage

Retirement planning starts with understanding that retirement accounts aren’t just places to park money — they’re TAX SHELTERS that the government literally incentivizes you to use.

We covered the basics in Section 5, but let’s go deeper here because this is CRITICAL:

The 401(k) — Your Workplace Superpower

If your employer offers a 401(k) with a match — that match is free money. Non-negotiable. Contribute at least enough to capture the full match before you do anything else financially. A typical 50% match on up to 6% of salary means an instant 50% return on that portion of your investment. Nothing in the market beats that.

Beyond the match, contributions are pre-tax — meaning they reduce your taxable income TODAY. If you earn $75,000 and contribute $10,000 to your 401(k), the IRS only taxes you on $65,000. That’s real, immediate savings.

The Roth IRA — The Long Game Champion

Pay taxes NOW on your contributions, and every dollar of growth comes out TAX-FREE in retirement. For younger investors especially, this is extraordinary. A 30-year-old who maxes out their Roth IRA ($7,000/year) consistently could realistically accumulate $700,000–$1,000,000+ in completely tax-free wealth by retirement age.

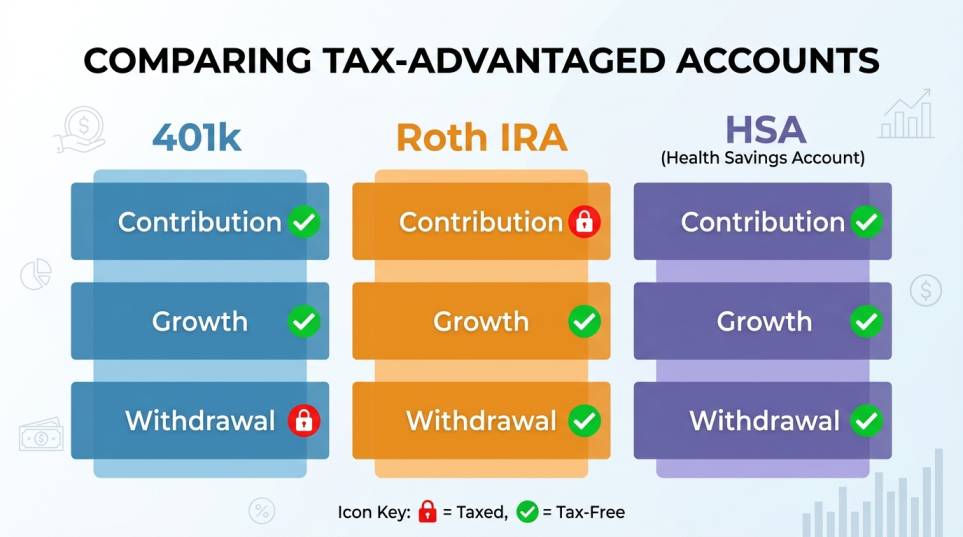

The HSA — The Hidden Triple Tax Advantage

If you have a high-deductible health plan, you qualify for a Health Savings Account (HSA) — and this is honestly one of the most underused tools in personal finance:

- Contributions are pre-tax (tax deduction now)

- Growth is tax-free

- Withdrawals for medical expenses are tax-free

Triple tax advantage. Fully legal. And after age 65, you can withdraw for ANY purpose (just pay regular income tax, like a 401k). Contribute the max — $4,150 for individuals, $8,300 for families in 2025 — and invest it aggressively inside the HSA.

Early Retirement Planning: The FIRE Strategy Explained

Early retirement planning has exploded in popularity over the last decade — largely through the FIRE movement (Financial Independence, Retire Early). And while retiring at 35 isn’t realistic for everyone, the PRINCIPLES behind FIRE are sound for anyone who wants more freedom sooner.

Here’s how FIRE calculates your retirement number:

Your FI Number = Annual Expenses × 25

This is based on the 4% Safe Withdrawal Rate — research showing that a portfolio can sustain 4% annual withdrawals for 30+ years without running out of money.

So if you need $48,000/year to live comfortably:

$48,000 × 25 = $1,200,000 is your financial independence target.

Hit that number — and you’re free.

FIRE variations to know:

| FIRE Type | Annual Spending Target | Lifestyle |

| Lean FIRE | Under $40,000/year | Frugal, minimalist living |

| Regular FIRE | $40,000–$80,000/year | Comfortable middle-class lifestyle |

| Fat FIRE | $100,000+/year | Comfortable with travel and flexibility |

| Barista FIRE | Partial — supplement with part-time work | Semi-retired with flexibility |

Pro Tip: Use the free FIRECalc calculator (firecalc.com) to model your specific retirement scenario — including your current savings, expected returns, planned spending, and target retirement year. It’s one of the most powerful free tools available for early retirement planning, and it takes under 5 minutes to run.

How to Reduce Your Tax Burden Legally — Right Now

You don’t need to wait until tax season to plan. Smart tax planning is a year-round habit:

- Max your 401(k) and IRA — the single highest-impact move for most people

- Harvest tax losses — sell underperforming investments to offset capital gains

- Hold investments long-term — qualify for the lower long-term capital gains rate (0%, 15%, or 20%) vs. short-term rates up to 37%

- Deduct business expenses — if you have a side hustle, track every legitimate business expense

- Work with a CPA — especially once your income grows, a good CPA pays for themselves many times over

Tools I recommend: TurboTax Premium for DIY filers with investment income, and TaxSlayer for straightforward returns at a lower cost. For anything complex — real estate, business income, multiple investment accounts — hire a CPA who specializes in investment or small business taxes.

8. Protect and Grow Wealth

Building wealth is one thing. KEEPING it — and growing it intelligently over time — is an entirely different skill set.

This is where wealth management comes in. And no, you don’t need to be a millionaire to think like one. The habits and systems that protect and grow wealth work at every income level. The earlier you build them, the more powerful they become.

Build Wealth Management Habits That Last

Wealth creation isn’t a single event — it’s a daily practice. The people who sustain and grow wealth over decades share a consistent set of habits. Here’s what that looks like practically:

1. Live Below Your Means — Always

No matter how much your income grows, keep your lifestyle inflation in check. Every raise, bonus, or windfall should be split — a portion toward lifestyle, the majority toward wealth-building. This single habit separates the wealthy from the high-income-but-broke.

2. Continuously Educate Yourself Financially

The financial landscape changes. Tax laws shift. New investment vehicles emerge. Markets move. Read one personal finance book per quarter. Follow credible financial voices. Stay informed — but filter aggressively. Not everyone with a finance TikTok account deserves your trust.

3. Review Your Financial Plan Quarterly

We’ll cover this more in Section 9, but the habit starts here. Wealth doesn’t manage itself. Schedule four financial reviews per year — 90-minute deep dives into your numbers, your progress, and your next moves.

4. Avoid Lifestyle Creep Aggressively

Lifestyle creep is what happens when income goes up and spending automatically follows — new car, bigger apartment, more dining out. It feels natural. But it silently kills wealth-building momentum. Automate your savings INCREASES alongside every income increase.

Preserve Wealth Over Time: Risk Management Essentials

Wealth preservation is the defensive side of personal finance — and most people completely ignore it until something goes wrong.

Here’s the truth: you can spend decades building wealth and lose significant portions of it in a single uninsured event, lawsuit, or market panic. Protection isn’t pessimism. It’s wisdom.

Insurance You Absolutely Need:

| Insurance Type | Why It Matters | Priority Level |

| Emergency Fund | First line of defense against all financial shocks | CRITICAL |

| Health Insurance | Medical bills are the #1 cause of personal bankruptcy in the US | CRITICAL |

| Term Life Insurance | Protects dependents if you die unexpectedly | HIGH (if you have family) |

| Disability Insurance | Replaces income if you can’t work — more likely than death before 65 | HIGH |

| Umbrella Insurance | Protects assets from lawsuits beyond standard policy limits | MEDIUM-HIGH |

| Homeowner’s/Renter’s Insurance | Protects physical assets and liability | HIGH |

Don’t panic-sell investments during market downturns. This is the single most wealth-destroying behavior among ordinary investors. Markets have recovered from EVERY crash in history — 2001, 2008, 2020 — and gone on to reach new highs. The investors who lost were the ones who sold in fear. The ones who held (and bought MORE during the dip) won.

Manage Investment Risk Intelligently

Smart wealth management isn’t about eliminating risk — it’s about managing it in proportion to your timeline and goals.

Key principles:

- Asset allocation by age — a classic rule: subtract your age from 110 to get your stock percentage. A 35-year-old = 75% stocks, 25% bonds/stable assets

- Rebalance annually — if stocks surge and now represent 85% of your portfolio, sell some and rebalance back to your target allocation

- Avoid concentrated positions — no single stock should represent more than 5–10% of your total portfolio

- Keep an “opportunity fund” — a small amount of liquid capital set aside to buy assets when markets dip

For more sophisticated wealth management beyond DIY, consider platforms like Betterment (automated rebalancing and tax-loss harvesting) or Vanguard Personal Advisor Services for hybrid human + automated advice at low costs. Once your investable assets exceed $500,000, engaging a fee-only fiduciary financial advisor is worth serious consideration.

Pro Tip: Always verify that any financial advisor you work with is a fiduciary — legally obligated to act in YOUR best interest, not earn commissions. Use NAPFA.org to find fee-only fiduciary advisors in your area. This one check could save you tens of thousands in misaligned advice over your lifetime.

9. Track Your Financial Independence Progress

Here’s a truth that doesn’t get said enough: a financial plan you never review is just a wish list.

Progress toward financial independence isn’t automatic — it needs to be measured, analyzed, and adjusted regularly. The people who actually REACH their financial independence goals aren’t the ones who set the best plans. They’re the ones who check in consistently and course-correct when life throws curveballs. And it will.

Net Worth Tracking: Your Most Important Financial Metric

Forget monthly income. Forget savings account balance. Your net worth is the single most accurate measurement of your financial health and progress toward independence.

Net Worth = Total Assets − Total Liabilities

Assets include: savings, investments, retirement accounts, real estate equity, business value, and any other owned assets.

Liabilities include: mortgage balance, car loans, student loans, credit card debt, personal loans.

Track this number monthly. You want to see it grow — even slowly — month over month, year over year. Some months it will dip (market corrections, unexpected expenses). That’s normal. The TREND over 12 months is what matters.

| Net Worth Milestone | What It Signals |

| Positive net worth | You own more than you owe — you’re building |

| 3–6 months expenses saved | Solid financial foundation established |

| 25× annual expenses | Classic financial independence target (the FI Number) |

| 33× annual expenses | Extra buffer — withdrawal rate drops to 3%, ultra-secure |

Best tools for net worth tracking:

- Empower (formerly Personal Capital) — Free. Connects all accounts automatically. Shows net worth, investment performance, and fee analysis in one dashboard. This is my top recommendation — it’s genuinely excellent

- Monarch Money — Cleaner UI, great for couples tracking joint net worth

- Tiller Money — Syncs your financial data automatically into Google Sheets or Excel — perfect for data lovers who want full control of their tracking

Savings Rate Tracking: The Pulse of Your FI Journey

Remember from Section 1 — your savings rate is the engine of financial independence. Track it monthly.

Monthly Savings Rate = (Amount Saved ÷ Gross Income) × 100

Include in “amount saved”: retirement contributions, brokerage transfers, extra debt payments, and cash savings.

Here’s a simple monthly tracking framework:

| Metric | This Month | Last Month | 12-Month Average |

| Gross Income | |||

| Total Expenses | |||

| Amount Saved/Invested | |||

| Savings Rate % | |||

| Net Worth | |||

| Passive Income Earned |

Copy this into a spreadsheet — or use the Tiller Money template which automates most of these fields for you.

Target benchmarks to aim for:

- 10–15% savings rate: You’re participating — keep pushing

- 20–30% savings rate: You’re building genuine momentum

- 40%+ savings rate: You’re on the fast track to financial independence

Investment Performance Review

Every quarter, spend 20–30 minutes reviewing your investment accounts. You’re not looking to react to short-term fluctuations — you’re checking:

- Are your contributions still on track?

- Is your asset allocation still aligned with your target?

- Are you paying unnecessary fees anywhere?

- Have any major life changes shifted your risk tolerance or timeline?

Watch your expense ratios closely. A fund charging 1% annually versus 0.03% (like Vanguard’s index funds) costs you an enormous amount over decades. On a $500,000 portfolio, that difference is nearly $5,000 per year in fees — silently draining your returns.

Monthly and Quarterly Financial Check-Ins

Build a consistent review cadence — this is where financial independence plans either hold together or quietly fall apart.

Monthly (30 minutes):

- Review spending vs. budget

- Record net worth

- Confirm savings and investment transfers happened

- Flag any unusual expenses

Quarterly (90 minutes):

- Full investment portfolio review

- Savings rate calculation and trend analysis

- Progress toward short and medium-term goals

- Tax planning check — are you on track with contributions?

- Review passive income performance

Annually (half-day):

- Full financial plan review

- Update net worth statement

- Reassess insurance coverage

- Review estate planning documents

- Set goals for the coming year

Adjust the Plan as Income and Goals Change

Life doesn’t stay static — and your financial plan shouldn’t either. Marriage, children, job changes, business income, windfalls, health events — all of these shift your numbers and your priorities.

The framework to follow when life changes:

- Income increases → Increase savings rate FIRST before lifestyle adjusts

- New debt acquired → Revisit the debt payoff section and reprioritize

- Market correction → Stay the course; review allocation but don’t panic

- Major life milestone → (Marriage, kids, inheritance) — do a full financial plan review

Pro Tip: Schedule your annual financial review as a recurring calendar appointment — same time every year, treated with the same seriousness as a doctor’s appointment. Call it your “Financial Independence Annual” and block the time months in advance. The investors and savers who consistently show up for their own financial reviews are the ones who actually cross the finish line.

Your plan is now complete — from goals to budget, debt to investing, passive income to tax strategy, wealth protection to progress tracking. Everything you need is here. The only variable left is YOU — and the decision to start.

Frequently Asked Questions About Financial Independence

What is financial independence and how do I know if I’ve achieved it?

Financial independence means your passive income and investment returns cover 100% of your living expenses — without needing to work actively for money. You’ve achieved it when your portfolio reaches your FI Number (annual expenses × 25) AND your investment income or passive streams consistently cover your monthly costs. It’s not a feeling — it’s a math equation you can verify. When the numbers line up and hold steady for 6–12 months, you’re there.

How much money do I need to save before I can retire early?

The standard formula is simple: multiply your expected annual expenses by 25. That’s your target. If you need $50,000/year to live comfortably, your early retirement target is $1,250,000. If you plan to live lean on $36,000/year, your target drops to $900,000. The lower your monthly expenses, the less you need — and the faster you get there. This is exactly why lifestyle choices matter as much as income when planning for early retirement.

What’s the 4% rule for financial independence?

The 4% rule comes from the Trinity Study — landmark research showing that a diversified investment portfolio can sustain annual withdrawals of 4% indefinitely without running out of money over a 30-year retirement period. So if your portfolio is $1,000,000, you can safely withdraw $40,000/year. It’s not a perfect guarantee — markets vary — but it’s the most widely accepted and historically tested benchmark in retirement planning. Many FIRE adherents use a more conservative 3.5% or 3% rate for extra security, especially if retiring before 50.

Should I pay off debt before investing for financial independence?

It depends on the interest rate — as we covered in Section 4. The practical rule: if your debt carries an interest rate above 8%, prioritize paying it off before investing beyond your employer’s 401(k) match. Below 8%, split your extra cash between debt repayment and investing simultaneously. The ONE exception is ALWAYS capturing your full employer 401(k) match first — that’s an instant 50–100% return nothing else can beat. Debt management and investing aren’t mutually exclusive; they’re a balancing act based on your specific interest rates.

How long does it take to achieve financial independence?

Honestly? It depends on three variables: your income, your savings rate, and your investment returns. At a 10% savings rate, you’re looking at roughly 35–40 years. For a 30% savings rate, closer to 20–22 years. At 50%+, potentially 10–12 years. The math is clear — the more aggressively you save and invest early, the faster you compress the timeline. There’s no universal answer, but there IS a universal principle: starting earlier always beats starting smarter. Every year you delay costs you compounding returns you can never fully recover.

What’s the difference between financial independence and retiring?

Great question — and the distinction matters. Retirement traditionally means stopping work entirely at a conventional age (65+). Financial independence simply means you have the OPTION to stop working — whether you exercise that option or not is completely up to you. Many financially independent people continue working — on projects they love, businesses they own, or causes they care about — simply because they want to, not because they have to. FI is about freedom. Retirement is one of many choices that freedom enables.

Can I achieve financial independence with a low income?

Yes — and I want to be direct with you here, because this question deserves a real answer, not false cheerfulness. It’s HARDER on a low income. It takes longer. It requires a higher savings rate relative to your income, which means tighter lifestyle choices. BUT — it is absolutely achievable. The key levers are: keep expenses exceptionally low, aggressively grow income over time (side hustles, skills development, career advancement), and invest consistently even in small amounts. Many people have reached financial independence starting from incomes under $40,000/year. The strategy doesn’t change. Only the timeline does.

What are the best investment vehicles for building financial independence?

In order of priority for most people pursuing financial independence: first, your employer’s 401(k) up to the full match. Second, a Roth IRA maxed annually (especially if you’re under 45). Third, a taxable brokerage account invested in low-cost index funds and ETFs like VTI, VXUS, and BND. Fourth, real estate — either direct ownership or REITs for more passive exposure. Finally, alternative income assets like dividend stocks, digital products, or online businesses. The common thread across all of these: low fees, diversification, and long time horizons. Investing for beginners starts with the first two — and for most people, those two alone will build life-changing wealth.

How do I calculate my net worth for financial planning?

Add up every asset you own: checking and savings accounts, investment and retirement accounts, real estate equity (current market value minus what you owe), vehicles, and any business value. Then subtract every liability: mortgage balance, car loans, student loans, credit card balances, personal loans. Assets minus liabilities equals your net worth. Use a free tool like Empower (Personal Capital) to automate this calculation by connecting all your accounts — it updates in real time and shows your trend over months and years. Review it monthly. Grow it intentionally.

What percentage of my income should I save?

The minimum baseline most financial experts agree on is 20% — the savings tier in the 50/30/20 budgeting rule. But if financial independence is your actual goal, push for 30–50% or higher. Even if you can only manage 10% right now, START there and increase by 1–2% every time your income grows. The percentage matters less than the HABIT. An automated $200/month investment at 25 years old beats a manual $2,000/month investment started at 45 — every single time, because compound growth is ruthlessly loyal to time. Save what you can. Increase it relentlessly.

Is financial independence possible in my 30s or 40s?

Absolutely — and more people are doing it than you might think. In your 30s, you have 20–30 years of potential compounding ahead of you, which is MORE than enough runway to build serious wealth if you start aggressively NOW. In your 40s, the timeline tightens, but it’s still very achievable — especially if your income has grown and you can save at a high rate. The Fat FIRE and Barista FIRE approaches are particularly popular among people starting their FI journey in their 40s, because they balance financial security with a realistic, enjoyable life in the meantime. The worst move in your 30s or 40s is deciding it’s “too late.” It’s not.

How do I build an emergency fund while investing?

Simultaneously — with a clear priority order. First, build a starter emergency fund of $1,000 as fast as possible. Second, capture your full employer 401(k) match (free money first, always). Third, grow your emergency fund to 3–6 months of expenses while making minimum debt payments. Fourth, once your full emergency fund is in place, shift that monthly savings toward maxing retirement accounts and investing aggressively. Don’t wait until your emergency fund is complete to start investing entirely — but DO make the starter fund your first financial goal. These two things can and should run in parallel once the foundation is in place.

Conclusion: Your Financial Independence Journey Starts with One Step

Let me leave you with something important — something I wish someone had told me clearly at the beginning of this journey:

Financial independence is not built by perfect people. It’s built by consistent ones.

You don’t need to nail every section of this guide simultaneously. No need for a six-figure salary to start. You don’t need to have it all figured out before you make your first move. What you need is a decision — followed by ONE action today, then another tomorrow, then another the day after that.

Look at what we’ve covered together in this guide. You now know how to define financial independence and calculate YOUR specific FI number. How to set short, medium, and long-term financial goals that are measurable and real. Now you have a framework for building a budget, choosing the right budgeting apps, and creating an emergency fund that actually protects you.

You understand how to approach debt management strategically — whether snowball or avalanche — and when to prioritize paying off debt versus investing for beginners. Now you have a clear picture of how to build an investment portfolio using index funds, ETFs, and tax-advantaged retirement accounts. You know what passive income really means, which ideas are genuinely worth your time, and how multiple income streams build the kind of resilience a single paycheck never can.

You’ve learned how tax planning and retirement planning can legally save you tens of thousands of dollars over your lifetime, and why wealth management and wealth preservation are the disciplines that protect everything you build. And you have a tracking system — net worth, savings rate, investment reviews, quarterly check-ins — that keeps your plan honest and moving forward.

That’s a complete financial independence blueprint. It’s all here.

Now — here’s your call to action, and I’m going to make it as simple as possible:

Pick ONE thing from this guide and do it TODAY.

Open a high-yield savings account for your emergency fund. Download YNAB or Empower and connect your accounts. Calculate your net worth for the first time. List your debts by interest rate. Set up a $50 automatic investment transfer into a Roth IRA.

It doesn’t have to be big. It has to be REAL.

Because the gap between people who achieve financial independence and people who dream about it isn’t talent, income level, or luck. It’s the willingness to start before they feel ready — and keep going when it feels slow.

Your future self — the one with options, freedom, and zero financial anxiety — is built by the version of you that starts TODAY.

Go build that life. You’ve got everything you need.